The Tax Most Hotels Misprice and Underpay

An independent hotel in Florence sells about 14,000 room-nights a year. Roughly half of those are taxable for the local tassa di soggiorno at EUR 5.80 per person per night for the property's category. Add the average occupancy of 1.7 guests per room and the maths gets to about EUR 70,000 a year of tourist tax that flows through the front desk, lives on the folio for somewhere between four hours and four months, and lands in the comune's bank account by the 15th of the following month. The line on the guest's bill is rarely more than 5 percent of the total stay. The exposure on the hotel's balance sheet is the entire EUR 70,000 plus whatever fines a missed filing earns. We have seen a 38-room boutique in Lucca pay a EUR 11,400 reassessment in 2024 for an exemption logic that was wrong since opening night in 2019, and the only reason the hotel could pay it without selling a vehicle is that the owner had been quietly building a reserve. The tax is small per guest. The accumulated cost of getting it wrong is not. The single biggest improvement an independent can make in a quarter is to put the whole stack on a PMS and accounting rail that captures, posts, reconciles, and remits every regime without a clerk doing it by hand at 23:30. The reconciliation and remittance side of that rail is exactly what hotel accounting software built around the PMS-to-GL bridge is supposed to do, and most independents are still doing it in a spreadsheet.

The collection side starts much earlier in the booking flow than most operators expect. The rate the guest sees on the booking engine and on the OTA must already be set up to either include or exclude the tourist tax depending on the regime. The folio at check-in must post the right amount per person per night, with the right exemption logic for children, business travellers, long stays, and (increasingly) hospital companions. The night audit must reconcile the posted total to the booking source. The accounting export must split the tax line into its own ledger account. None of this is exotic technology. It is the daily work of a hotel property management system that owns the booking, the folio, and the accounting handover end to end. This article is the honest 2026 country-by-country picture of what that work looks like for an independent operating in any of the major European regimes, the twelve operational failures that earn fines and audits, and a 21-day plan to clean up an existing property without paying for an outside compliance consultant.

I write for Prostay, the team that runs this rail across roughly 1,200 Italian comuni, the entire French taxe de séjour catalogue, the Berlin and Hamburg city-tax regimes, every Catalan and Balearic municipality with a tasa turística, and the major Portuguese cities that charge a taxa municipal turística. The numbers, deadlines, and operational failures below come from the published regulations, our integrations team's running notes on every change since 2023, and the actual audit notices our customers received in 2024 and 2025. There is no harmonisation on the horizon. The eIDAS-driven invoice-format unification effort has not even started a working group on tourist tax. In the meantime the work is country by country, region by region, comune by comune, and the only sustainable answer is to put it on automation and check the matrix every quarter.

What Tourist Taxes Actually Are (and Are Not)

Tourist tax is the catch-all English label for a family of local levies collected by accommodation operators on behalf of municipalities, regions, or (rarely) national governments. The label hides a lot of variation. The hotel collects from the guest at check-in or check-out, holds the cash on its own balance sheet for the remittance window, files a return on the regulator's clock, and remits the cash net of any banking fees the regulator allows the operator to deduct.

What tourist tax is not: a value-added tax, a service charge, a national tax, a fee for a regulator-issued service, or revenue the hotel ever owns. The cash sits on the hotel's books as a payable, not as revenue, from the moment of charge posting to the moment of remittance. Treating it as revenue inflates the income statement, distorts RevPAR, and creates a tax-on-tax exposure when the local accountant inadvertently includes it in the VAT-able base. The first audit point inspectors check in 2025 inspections, in our customers' experience, is the chart-of-accounts mapping for the tourist tax line: it should land in a dedicated short-term liability account (typical chart-of-accounts code 2310 or similar), not in any 4xxx revenue account.

The other persistent confusion is between tourist tax and the various business-purpose, environmental, or city-marketing levies that have proliferated in the past five years. Venice's day-tripper access fee introduced in 2024 is not a tassa di soggiorno; it applies to non-staying visitors and is collected by the comune directly. Greece replaced its 2018 overnight tax with a Climate Crisis Resilience Levy in late 2024. The Netherlands' Amsterdam toeristenbelasting is the highest in Europe at 12.5 percent of room rate from 2024 onwards. Each of these is operationally separate from the EU's older tourist-tax pattern and needs its own posting rule.

The Twelve Operational Failures That Trigger Audits

Across the reassessment letters and audit notices our customers actually received in 2024 and 2025, the same twelve failures account for almost every euro of penalty. They are listed in descending order of frequency, with the operational fix.

- Wrong rate after a regulator update. A municipality raises the tassa di soggiorno from EUR 4.00 to EUR 5.00 for 4-star hotels effective 1 March, the operator's PMS rate is still EUR 4.00 on 1 May, and the gap is the audit. Fix: a quarterly review of every regime's published rate, plus an automated alert when the regulator publishes an amendment.

- Children exemption applied wrong. The most common version is a hotel that exempts every minor under 18 across all regimes, when in fact Rome exempts under 10s and Lisbon exempts under 13s. Fix: a per-regime exemption matrix in the PMS, applied automatically off the date-of-birth field on the registration record.

- Long-stay cap not applied. Italy and Catalonia cap the taxable nights at 7 (some Italian comuni at 3 or 5). A guest staying 14 nights pays for the first 7 and gets a zero-rate posting for nights 8 to 14. Properties on flat-cap rules without the per-regime variant overcharge or undercharge by hundreds of euros per long stay. Fix: per-regime cap parameter in the posting rule, with an automated test against a 14-night sample.

- Business-traveller exemption missing in Germany. Berlin's ÜSG, Hamburg's Übernachtungsteuer, and the various Bettensteuer regimes exempt business travel. The traveller signs an Arbeitgeberbestätigung; the hotel files the form with the monthly return. Hotels that never collect the form charge business travellers wrongly and refund on dispute, or worse, never refund and absorb the dispute as bad debt. Fix: a digital business-purpose declaration in the booking engine for German bookings, with a back-up paper form at the front desk.

- OTA-collected portion double-paid. Booking.com remits the tax to the commune directly; the hotel also posts and remits the same tax. The result is a 2x payment to the regulator and a refund cycle that takes 9 to 14 months in Italy. Fix: the channel manager flags the OTA-collected reservations and the PMS posting rule produces a zero-amount line for the same reservation, preserving the reporting record without producing a duplicate cash payment.

- Filing a regime where the cash flow was zero. A small French commune where the entire stay was OTA-collected still expects the hotel's quarterly declaration. Operators skip the filing because nothing changed, and the missing declaration is the audit trigger. Fix: file every regime every cycle, even when the cash collected by the hotel is zero, with a clear note explaining the OTA channel.

- Wrong VAT treatment. The local accountant includes the tourist tax in the VAT-able base, the hotel pays VAT on a payable, and the cumulative overpayment is six figures across a multi-year window. Fix: a one-page tax matrix per country, signed by the local accountant once a year, taped to the inside of the back-office cabinet.

- Refund logic broken on no-shows and cancellations. A no-show was charged the room rate, and the tourist tax was posted on the folio, but the regulator's rule excludes no-shows from the taxable base. The hotel pockets a 5-euro line that legally belongs to the guest. Fix: a posting reversal triggered by the cancellation/no-show flag, plus a quarterly check on the no-show ledger.

- Group bookings with mixed exemption categories. A 40-person tour with 2 children, 1 person with a disability companion, 35 paying adults. The hotel posts the same line for everyone. Fix: a per-guest folio split that captures exemption category at registration and posts only the taxable subset.

- Late filing past the comune-specific deadline. Most Italian comuni file by the 15th or 16th of the following month; Berlin's Stadtkasse takes the 10th of the second following month; Catalonia files quarterly. Properties with two or more regimes typically miss one a year. Fix: a single accounting calendar with each regime's filing deadline plotted, plus an automated reminder 5 working days before each.

- Bank reconciliation not run on the remittance. The hotel files the return showing EUR 6,400 due, the bank transfer is for EUR 6,400, but the bank statement shows EUR 6,395 because of a EUR 5 wire fee the regulator does not absorb. The 5-euro shortfall accrues interest and shows up in the next audit as an unsettled balance. Fix: a reconciliation step that ties the bank-statement line to the filed amount, with a separate G/L line for any wire fee.

- No retention of the filed return and acknowledgement. The audit window is 3 to 10 years depending on country (5 years Italy, 3 years France, 4 years Germany, 4 years Spain, 4 years Portugal). Hotels that lose the filed return PDFs cannot defend the return values during an audit, even if the bank statements show correct cash flow. Fix: a single archive folder per regime per year, holding the filed return PDF, the regulator's acknowledgement, the bank-statement line, and the underlying G/L extract.

Country Playbooks

Six regimes worth a dedicated section, plus a quick tour of Greece, Austria, the Netherlands and Belgium. Each playbook is structured the same way: legal basis, where it applies, the rate range, who is exempt, the filing platform, the deadline, the penalty schedule, and the failure mode we see most often.

Italy: La Tassa di Soggiorno (per Municipality)

Legal basis: Decreto Legislativo 23/2011, art. 4. Each comune institutes its own regulation under the framework, with rates capped at EUR 5.00 per person per night, raised in select capital and art-cities to as high as EUR 10.00 per person per night for top-category hotels. The regime is one of the oldest and broadest in Europe.

Where it applies: roughly 1,200 of Italy's 7,900 comuni operate a tassa di soggiorno, including all major tourist destinations. Rome, Florence, Venice, Milan, Naples, Bologna, Turin, Genoa, Verona, Pisa, Siena, Perugia, Catania, and most of the Amalfi and Cinque Terre coast.

Rate range 2026: EUR 1.00 to EUR 10.00 per person per night, by hotel category and comune. Rome 2024-2026: EUR 4.00 (1-star) to EUR 10.00 (5-star). Florence 2025-2026: EUR 1.00 to EUR 8.00. Venice 2025-2026: EUR 1.00 to EUR 5.00 plus a separate day-tripper access fee for non-staying visitors. Milan 2026: EUR 2.00 to EUR 5.00. Most comuni publish their tariffario in a deliberazione di giunta that updates 1 January (sometimes 1 March).

Exemptions: under-10s in Rome; under-12s in Florence; under-18s in Milan; under-6s in Venice with a reduced rate 6 to 13. Patients and accompanying companions in hospitals, drivers and tour-coach personnel, government inspectors. Long stays beyond the comune's cap (3, 5, 7, 10, or 14 nights depending on the comune).

Filing platform: per-comune. Rome uses SOLE Roma Capitale, accessed at portale.soleroma.it. Florence uses the comune's tributi portal. Venice uses the Venezia Unica portal. Most smaller comuni accept a paper form or PEC e-mail with the spreadsheet attached. Larger comuni publish an XML schema for PMS direct integration; SOLE in Rome accepts an OAuth-secured API submission since 2023.

Deadline: typically the 15th or 16th of the month following the stay. Rome: 16th. Florence: 15th. Venice: monthly within 16 days. A small number of resort comuni file quarterly.

Penalties: D.Lgs. 471/97 omitted-payment regime, plus comune-level surcharges. Late payment: 30 percent of the unpaid amount, halved to 15 percent if cured within 90 days, or to 1.50 percent under ravvedimento operoso if cured within 14 days. Late filing: EUR 25 to EUR 250 per filing. Falsified declarations: criminal exposure under art. 5 D.Lgs. 74/2000 if the threshold is crossed.

The failure we see most: hotels treating the cap mechanically. A 6-night stay in Rome where the cap is 10 nights: cap not relevant. A 14-night stay in Rome: only first 10 nights taxable, and the PMS posting must zero-rate nights 11 to 14. A 12-night stay in Venice: only first 5 nights taxable. Properties that do not parametrise the cap by comune end up either over-collecting (refund liability) or under-collecting (assessment liability) depending on how the property's heuristic was set up.

France: La Taxe de Séjour and the télédéclaration Platforms

Legal basis: Code général des collectivités territoriales (CGCT), articles L2333-26 to L2333-46-1, plus the 2019 loi pour un tourisme durable that introduced collect-on-behalf for digital intermediaries.

Where it applies: roughly 5,000 of France's 35,000 communes operate a taxe de séjour. Paris, the entire Côte d'Azur, the major Atlantic coast resorts, the Alps and Pyrenees ski stations, the Loire Valley wine region, Bordeaux and the Médoc, the Lyon and Strasbourg metro areas. Many communes pool collection through their EPCI (intercommunalité).

Two regimes: au réel (per night per person, the modern default) and forfaitaire (a flat amount per accommodation per night, used by a shrinking minority of small communes). Almost every meaningful tourist destination uses the réel.

Rate range 2026: EUR 0.20 to EUR 5.00 per person per night for classified accommodations (1-star to palace), set per commune within the CGCT-published tariff. Unclassified or non-rated accommodations: 1 to 5 percent of the published nightly rate, capped at EUR 5.00 per person per night, plus a regional surtax (taxe additionnelle départementale, plus the Île-de-France surcharge in Paris and the Greater Paris region). Paris 2024-2026: a palace pays EUR 14.95 per person per night including the regional and departmental surtaxes.

Exemptions: under-18s nationwide. Seasonal workers under contract on the property. Persons receiving emergency social housing. Long stays where the accommodation is the primary residence.

Filing platform: OFTour (Open Source Taxe de Séjour) and OFFRE are the two most-used aggregator platforms. Many communes built their own portal: DECLOC for the Côte d'Azur cluster, MERIT for the Alpes Maritimes EPCI, Taxesejour.fr for a large group of resort communes. Paris filings go through the Mairie de Paris portal. The 2019 reform forces every commune to accept a télédéclaration channel; paper filing is being phased out by 2027.

Deadline: quarterly is the most common cycle, with monthly cycles in higher-volume communes. The standard quarterly deadlines are 30 April, 31 July, 31 October, 31 January.

Penalties: missing declaration EUR 750 fine per missing return (CGCT art. R2333-58). Late payment: 10 percent surcharge plus default interest under the general tax code. False declaration: contravention de la 5e classe up to EUR 1,500 per false statement.

The failure we see most: misclassifying the property between classified and unclassified categories. A boutique hotel that lost its Atout France classification in 2022 and never re-applied is technically unclassified for taxe de séjour purposes, which means the rate base flips from a flat tariff to a percentage of nightly rate. A property continuing to charge the EUR 1.65 flat rate when it should be charging 5 percent of the EUR 220 ADR (about EUR 11.00) is undercollecting by EUR 9.35 per person per night, and the audit window is 3 years.

Germany: Bettensteuer, City Tax, and Kurtaxe

Legal basis: Kommunalabgabengesetze (KAG) at Land level, plus the per-municipality Übernachtungssteuersatzung (Berlin's ÜSG is the marquee example). The Bundesverfassungsgericht's 11 July 2012 ruling drew the line between Bettensteuer (leisure only, by federal court order) and Kurtaxe (every overnight stay in designated Kurorte, regardless of business purpose).

Where it applies: Bettensteuer in Berlin, Hamburg, Frankfurt, Cologne, Munich (from 2025), Bremen, Hannover, Leipzig, Dortmund, Düsseldorf, Stuttgart, Nuremberg, Mannheim, Mainz, and a growing list of mid-sized cities. Kurtaxe in approximately 350 designated Kurorte across Bavaria, Baden-Württemberg, Lower Saxony, Mecklenburg-Vorpommern, Schleswig-Holstein, and Thuringia.

Rate range 2026 (Bettensteuer): Berlin 7.5 percent of the net room rate, capped at 21 nights per stay. Hamburg EUR 0.50 to EUR 4.00 per night sliding by net price tier. Frankfurt 2 percent of the net room rate. Cologne 5 percent of the net room rate. Munich (from 1 January 2025) 5 percent of the net room rate. Most rates apply to leisure stays only.

Rate range 2026 (Kurtaxe): typically EUR 1.50 to EUR 4.00 per person per night, by season and by Kurort. Bad Reichenhall, Baden-Baden, Norderney, Sylt, and Berchtesgaden run on the upper end of this range. Stacks with the local Bettensteuer where both apply.

Exemptions: Bettensteuer applies to leisure travel only after the 2012 ruling. Business travellers must produce an Arbeitgeberbestätigung (employer declaration) at check-in or shortly after; the form lives with the hotel for the audit retention period. Children under 18 are exempt in Berlin, Hamburg, Frankfurt, Cologne, and Munich; some cities exempt only under-12s. Kurtaxe applies to every overnight stay regardless of business purpose, with limited exemptions for terminally ill patients and seasonal workers under contract.

Filing platform: per-municipality Stadtkasse. Berlin's portal accepts a structured XML upload from PMS systems since 2022, plus a manual Excel template. Hamburg uses the Bundesportal-like Stadtkasse interface. Cologne and Frankfurt accept PEC-equivalent structured e-mail with attached Excel. Smaller cities still file via paper or e-mail.

Deadline: monthly for the major cities. Berlin's ÜSG: 10th of the second following month. Hamburg: 15th of the following month. Frankfurt and Cologne: 15th of the following month. A small number of cities run quarterly, including the Munich 2025 launch.

Penalties: §378 Abgabenordnung Steuergefährdung, fines up to EUR 25,000 per breach. The Berlin Verwaltungsgericht has confirmed in 2024 case law that a hotel without a documented business-purpose verification process is presumed to have charged correctly only to leisure travellers, which means missing Arbeitgeberbestätigungen create a positive assessment of unpaid tax.

The failure we see most: hotels conflating Bettensteuer and Kurtaxe in the PMS posting rule, and creating a single posting code that charges every guest a single line. The cleanest architecture is two separate posting rules per property: one for Bettensteuer (gated on leisure flag plus net rate base, applied in cities where Bettensteuer is operative), one for Kurtaxe (applied in Kurorte regardless of leisure status). A property that runs both regimes (a hotel in Bad Reichenhall, for example) needs two posting lines on the folio, two G/L accounts, and two filings per month.

Spain: Tasa Turística in Catalonia, the Balearics, and Beyond

Legal basis: regional, not national. Catalonia operates the Impost sobre les estades en establiments turístics (IEET) under Llei 5/2012. The Balearic Islands operate the Impuesto sobre Estancias Turísticas (ITS) under Llei 2/2016. Other regions have draft or partial regimes; Valencia announced and then suspended a tasa turística in 2024, Canarias began rollout in 2025 with municipality-level rates in Tenerife and Lanzarote.

Where it applies: every commercial accommodation in Catalonia and the Balearic Islands. Hotels, hostels, vacation rentals, agroturismes, campsites. Some regions exempt very small operators under a threshold (Catalonia: properties with under 5 rooms; Balearics: similar threshold).

Rate range 2026 (Catalonia): EUR 1.10 to EUR 3.50 per person per night for the regional IEET, capped at 7 nights per stay. Barcelona adds a regional recargo (surcharge): EUR 4.00 in 2024, EUR 5.00 in 2025, EUR 6.00 from 2026. The Barcelona total for a 5-star property in 2026 is EUR 9.50 per person per night for the first 7 nights.

Rate range 2026 (Balearic Islands): EUR 1.00 to EUR 4.00 per person per night, by category and season. The Balearic ITS doubles in high season (May to October) and is reduced or exempt in the low-season shoulder. Children under 16 exempt.

Exemptions: under-16s in Catalonia and Balearics. Long stays beyond 7 nights (the cap, not full exemption). Stays at sociosanitary establishments. Catalonia also exempts stays for natural-disaster relief and journalists on official assignment.

Filing platform: Catalonia uses the Agència Tributària de Catalunya (ATC) portal, with the IEET filed via Modelo 950 (quarterly) and Modelo 940 (annual summary). The ATC accepts electronic filing only since 2020. The Balearic ITS files through the ATIB portal on a quarterly cycle, with annual reconciliation.

Deadline: quarterly. Catalonia: between 1 April and 20 April for Q1, then 1 July to 20 July, 1 October to 20 October, and 1 January to 20 January. Balearics: similar quarterly window with a short grace period.

Penalties: under the Spanish Ley General Tributaria 58/2003, infracciones leves carry 50 to 100 percent of the unpaid amount, infracciones graves 100 to 150 percent, infracciones muy graves 150 to 300 percent. Late filing without unpaid tax: EUR 100 to EUR 200 per filing under art. 198 LGT. The catalan Agència Tributària also publishes a recargo for late payment on top of the LGT regime.

The failure we see most: hotels treating the Barcelona recargo as part of the IEET rate. The recargo is a separate municipal surcharge with a separate G/L account and a separate item on the filing. A property that posts a single combined line to its IEET ledger account ends up with a chart-of-accounts mismatch on filing day, and either over-files the IEET or under-files the recargo. The cleanest setup is two posting codes on the folio for Barcelona properties, with two G/L accounts and a clean reconciliation per quarter.

Portugal: Taxa Municipal Turística

Legal basis: article 119-A of the Regime Financeiro das Autarquias Locais (Lei 73/2013) plus per-municipality regulamentos. The taxa is collected by the operator and remitted to the município.

Where it applies: Lisbon, Porto, Cascais, Sintra, Mafra, Faro, Lagos, Albufeira, Évora, Madeira (Funchal), and a slowly growing list of secondary tourist municipalities. Each município sets its own rate.

Rate range 2026: Lisbon EUR 4.00 per person per night (raised from EUR 2.00 in September 2024). Porto EUR 3.00 per person per night. Cascais and Sintra EUR 2.00. Faro and the Algarve municipalities EUR 1.00 to EUR 2.00. Madeira EUR 2.00 in Funchal.

Exemptions: under-13s in Lisbon, under-12s in Porto. Stays beyond the 7-night cap (Lisbon, Porto). Patients and accompanying companions in hospitals.

Filing platform: per-município. Lisbon uses the Câmara Municipal de Lisboa portal (CML) with electronic submission since 2022. Porto operates a similar portal at the Câmara Municipal do Porto. Smaller municipalities accept paper or PEC-equivalent submissions.

Deadline: monthly within 15 days of the month-end (Lisbon, Porto), quarterly for some smaller municipalities.

Penalties: contraordenação tributária under the Regime Geral das Infrações Tributárias (RGIT). Late filing or missing declaration EUR 75 to EUR 3,740 per breach. Cumulative interest on unpaid amounts.

The failure we see most: properties that did not raise the Lisbon rate from EUR 2.00 to EUR 4.00 on the September 2024 effective date. The undercollection is EUR 2.00 per person per night across the entire post-September stay book. For a 60-room hotel running 75 percent occupancy, that is EUR 25,000 to EUR 35,000 of underpayment per quarter, plus the audit penalty regime. The CML's audit cycle picked up several of these in early 2025 and the reassessment letters arrived in March 2025.

Greece, Austria, the Netherlands, and Belgium in Ninety Seconds

Greece: the 2018 overnight stay tax (Φόρος Διαμονής) was replaced from 1 October 2024 by a Climate Crisis Resilience Levy (Τέλος Ανθεκτικότητας στην Κλιματική Κρίση), at EUR 1.50 to EUR 10.00 per room per night by accommodation category and season. The new levy is per room, not per person; the operator files monthly to the AADE (the Greek tax authority) and remits the cash. Penalties under the Greek Tax Procedures Code: 50 percent of unpaid amount minimum.

Austria: Ortstaxe (Vienna) and Tourismusabgabe at Land level. Vienna applies a 3.2 percent levy on the net room rate. Salzburg and Tyrol apply per-person nightly rates from EUR 1.50 to EUR 3.50. Filing per-Land or per-municipality, monthly. Children under 15 exempt in Vienna, with variation by Land.

Netherlands: toeristenbelasting per municipality. Amsterdam runs the highest rate in Europe at 12.5 percent of the net room rate from 2024 onwards. Rotterdam 7 percent. The Hague 6.5 percent. Filing typically annual or quarterly. The unusual feature: in some Dutch municipalities the toeristenbelasting is treated as part of the supply for VAT purposes, which means the operator must split the published nightly rate between the room base, the VAT, and the toeristenbelasting carefully.

Belgium: Brussels city tax of EUR 4.24 per person per night (the published 2024-2026 rate, updated annually for inflation). Antwerp city tax EUR 2.69. Bruges EUR 2.83. Filing monthly or quarterly per commune. Belgium and Luxembourg occasionally treat the tax as VAT-able; check the local accountant.

How to Set Up Charge Posting in Your PMS

The single biggest leverage point in a tourist-tax stack is the PMS posting rule. Done right, every check-in posts the right line to the folio with no manual intervention; the night audit picks up the line into the daily revenue report; the accounting export sends it to the tax-payable G/L account. Done wrong, the front desk runs a manual override every shift and the audit trail looks like Swiss cheese.

The right setup has six elements. One, a per-property regime selector that maps the property to one or more tax regimes (a Barcelona hotel sits under IEET plus the Barcelona recargo; a Bad Wörishofen hotel sits under both Bettensteuer and Kurtaxe; a property in a non-tax-zone has the regime selector empty). Two, a per-regime rate table that captures the published tariff and the effective dates, indexed by hotel category and (where relevant) by season. Three, a per-regime exemption matrix: under-x age, business-purpose, hospital companion, long-stay cap, seasonal worker. Four, a posting trigger that fires on either check-in (the most common pattern) or each night-audit cycle (cleaner for stays that span a rate change). Five, a posting code that lands the line on a dedicated G/L account, never on a revenue account. Six, a reversal trigger on cancellation or no-show that zeros the line cleanly without leaving a phantom in the audit log.

The two parameters most operators tune incorrectly are the posting trigger and the rate-change rule. A posting trigger that fires once at check-in but does not split a stay across a rate change date (e.g. a stay running 30 December through 5 January when Lisbon raises the rate on 1 January) ends up under-posting or over-posting depending on which side of the change the trigger fires. A posting trigger that fires nightly at audit time handles the rate change cleanly but creates more accounting lines per stay. Either pattern works as long as the property documents which it uses and tests the boundary case in the rate-change quarter.

Test the setup by running a known-quantity sample through the system before go-live: a 7-night stay with two adults and one child of the relevant exempt age, a long stay that crosses the cap, a business stay that requires the German Arbeitgeberbestätigung, an OTA reservation pre-collected by Booking.com, a no-show, a stay with a refund partway through. Compare the posted total against a hand-calculated total. Iterate until the difference is zero. Most properties find at least one bug in the rule on the first pass.

How to Set Up Reconciliation in Your Accounting System

The accounting half of the stack catches anything the PMS missed. The required pieces, in roughly the order an external auditor will check them.

A dedicated G/L account per regime, sitting in the short-term liability range of the chart of accounts. Italian charts often use 2310 for tassa di soggiorno raccolta, with sub-accounts per comune for multi-property groups. French charts use 4471 (or a 4xx subaccount) for taxe de séjour en attente de reversement. German charts use a Verbindlichkeiten account in the 1700-1799 range, distinct from VAT. The point is not the specific code; it is that the line never touches a revenue account.

A daily transfer from the PMS posted-line to the G/L account, with the line preserving the booking reference, the guest reference, the regime tag, and the night reference. The transfer should be automatic on the night-audit cycle, not a manual export the back office runs at month-end. The night-audit transfer is the moment where reconciliation between the PMS and the G/L should be perfect; any difference at this point is a bug to fix before it compounds.

A monthly reconciliation against the regulator's filing. The flow is: pull the month's G/L balance for the regime, run the PMS report for the same month, run the regulator's pre-fill (if available; many regulators echo the prior filings back to the operator), confirm the three numbers agree, file. The reconciliation step catches the wire-fee gap, the OTA double-pay risk, and any rate-change boundary case. Hotels that skip this step learn about the discrepancy 18 months later in a reassessment letter.

A bank-statement match against the remittance. Every monthly or quarterly remittance lands as a single line on the bank statement (or a small handful of lines if the regulator splits by stay-month or by property). The bank reconciliation should map each line to the corresponding filing, with a sub-line for any wire fee or banking surcharge that should not have been deducted from the principal.

An archive folder per regime per fiscal year, holding the filed return as a PDF, the regulator's acknowledgement (if issued), the bank-statement line, the underlying G/L extract, and the PMS posting report. The folder should survive the audit window of the longest-statute regime in the property's portfolio: 5 years for Italian filings, 4 for German, 4 for Spanish, 3 for French, 4 for Portuguese. A multi-country group's defensive retention is 10 years for tax-evasion exposure under §§ 169-170 AO in Germany.

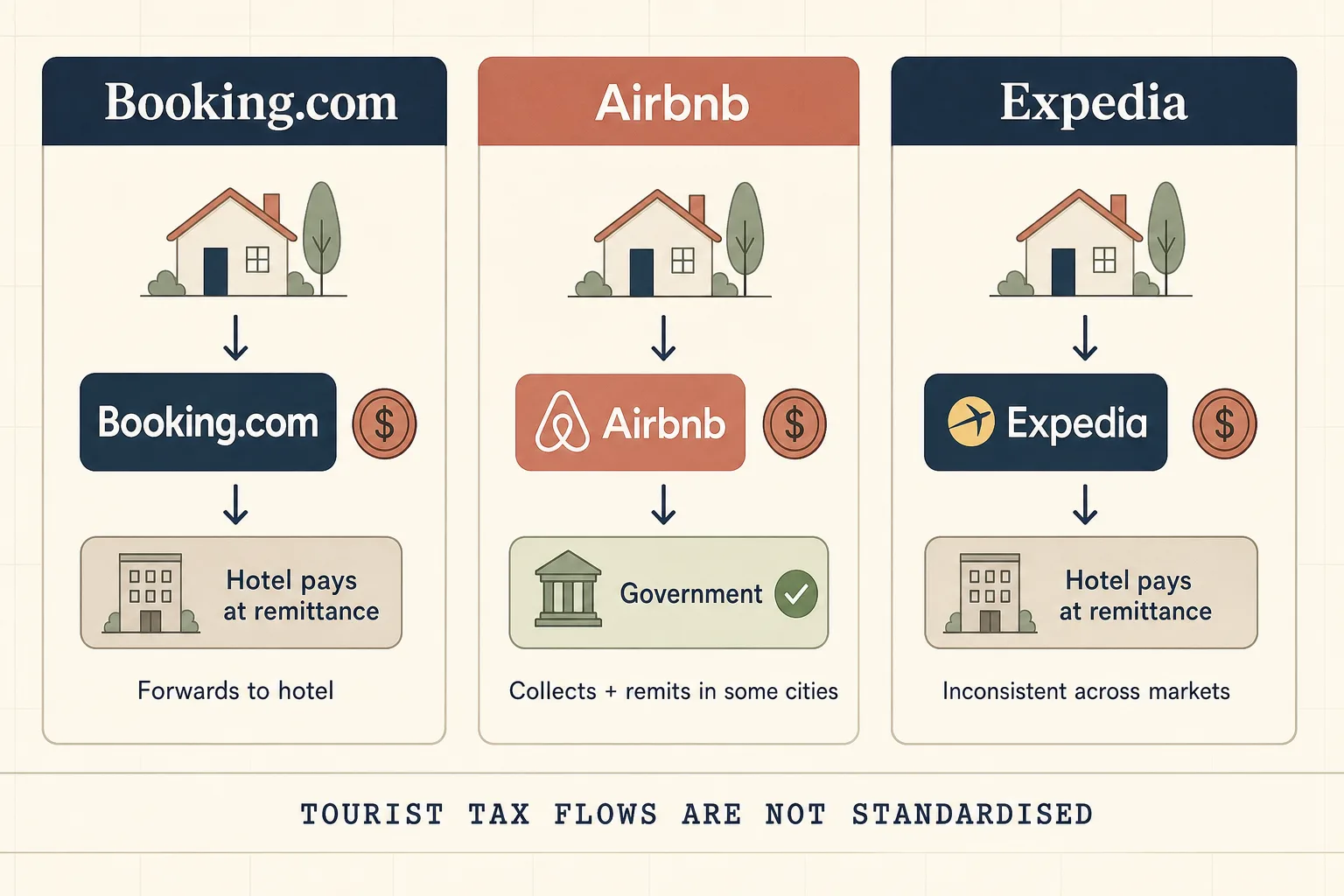

The OTA Problem: Booking.com, Airbnb, and Tax Withholding

The single most confusing operational change in the past five years is the OTA collect-on-behalf reform, which started in France in 2019 and has now propagated to roughly half the regimes covered above. The pattern is the same in every regime: the digital intermediary (Booking.com, Airbnb, Expedia for some properties, Vrbo for vacation rentals) withholds the tourist tax from the booking, passes the room rate to the hotel net of the withheld tax, and remits the tax directly to the regulator on a timetable that does not align with the hotel's filing cycle. The hotel ends up with three separate streams of cash flow: bookings where the OTA collected and remitted, bookings where the OTA collected but only handed the cash to the hotel for forwarding, and bookings where the hotel collected directly.

The cleanest architecture treats each stream as a separate ledger column. Stream 1: OTA collected and remitted. The hotel posts a zero-cash line to the folio (preserving the reporting record) and files the tax as a notional volume number on the return, with the OTA's remittance attestation as supporting evidence. The cash never touches the hotel's bank account. Stream 2: OTA collected and forwarded. The hotel receives the cash from the OTA, holds it in the standard tax-payable G/L account, and remits to the regulator on the regulator's clock. This is the case in some Italian comuni where the comune has not yet signed a collect-on-behalf agreement with Booking.com. Stream 3: hotel collected directly (the historical default). Direct bookings, walk-ins, group contracts, corporate accounts. The hotel runs the standard collect-post-remit cycle.

The two operational failures we see in the OTA stream are double-payment and underpayment. Double-payment happens when the channel manager does not flag the OTA-collected reservation correctly and the PMS posts the standard tax line on top of the OTA's silent withholding. The hotel pays the regulator twice; the refund cycle is 9 to 18 months in our experience across Italian and French municipalities, and it is rarely settled without an explicit dispute. Underpayment happens when the channel manager does flag the OTA-collected reservation but the filing template does not include the OTA volume in the gross declaration, which means the regulator sees a lower volume than the OTA's remittance, the numbers do not reconcile at the regulator's end, and the audit trigger fires the next quarter.

The clean defensive practice is to file the gross volume on every return, with a clear breakdown showing OTA-collected vs. hotel-collected, and to remit the cash that came through the hotel's bank account. The regulator's reconciliation tool then matches the OTA's parallel remittance against the gross volume and the cycle closes. Hotels that file only the hotel-collected volume, omitting the OTA-collected portion, look like they are underreporting and frequently get audited even when the regulator's actual cash position is whole.

VAT Treatment: Why Tourist Tax Is (Usually) Not VAT-able

The dominant rule in every major EU regime: the tourist tax is excluded from the VAT-able base. The hotel's invoice shows the room rate, the VAT on the room rate at the relevant rate (10 percent in Italy, 10 percent in France, 7 percent in Germany, 10 percent in Spain, 6 percent in Portugal under hotel-specific rates), and the tourist tax as a separate line with no VAT line of its own. The Italian Agenzia delle Entrate confirmed the rule in resoluzione 110/2015 and has not revisited it. The French DGFiP confirmed the same in BOI-TVA-CHAMP-10-10-50 and has not revisited it. Germany's Bundesfinanzministerium addressed the question in 2014 and again in 2020 and confirmed the rule for Bettensteuer and Kurtaxe.

The two notable exceptions: Belgium and the Netherlands treat the tourist tax as part of the supply for VAT purposes in some municipalities, which means the published nightly tax rate becomes inclusive of VAT and the hotel has to split it on the invoice. A property in Amsterdam (12.5 percent toeristenbelasting on the net room rate) is in a different posture from a property in Lisbon (EUR 4.00 flat per person per night, separate from VAT).

The defensive operational practice is a one-page tax matrix per country that the local accountant signs once a year. The matrix lists the regimes operative at the property, the published rate, the VAT treatment, the filing platform, the deadline, and the G/L account. The matrix lives in the back office and updates only when the regulator publishes an amendment. Most hotels do not have this matrix; the ones that do close their audits in under a working day, and the ones that do not spend two weeks reconstructing the rule from old e-mails.

The Monthly and Quarterly Remittance Cycle

The cycle that most often breaks is June. Italian and Portuguese filings cluster around mid-June for the May stay month; French quarterly filings due 31 July; Spanish quarterly filings due 20 July; German monthly filings due 10 or 15 July. A property running three or more regimes hits four to six separate filing deadlines between mid-June and late July, often with overlapping cash-flow windows. We see more late filings in this cluster than in any other month of the year.

The defensive practice is a single accounting calendar that plots every regime's deadline in advance, with a 5-working-day reminder ahead of each. The calendar is a shared resource, owned by the controller or the operations manager, with the regime, the cycle (monthly or quarterly), the deadline date, the filing portal URL, the credentials reference, the typical cash position at filing time, and the accountant or external advisor on retainer for that regime.

Cash flow is the second-order failure. Tourist tax cash sits on the operator's books from the moment of collection at check-in to the moment of remittance, which can be a 45-day window for monthly regimes (collection on 1 June, remittance by 15 July) and a 110-day window for quarterly regimes (collection on 1 January, remittance by 20 April). For a 60-room property running EUR 70,000 a year of tourist tax, the working-capital exposure is about EUR 8,000 to EUR 22,000 sitting on the balance sheet at any given moment. This is normal but it is not free; the cash needs to be visible in the rolling cash forecast and the filing reminder needs to fire 5 working days before the bank transfer is needed.

The 21-Day Cleanup Playbook

A 21-day plan to take an existing property from "we file, but we are not sure we file correctly" to "we have a clean rail across every regime that applies to us." One operations-minded person can run this; expect 4 to 6 hours a week from the front-desk lead and the controller for the duration.

Days 1 to 3: scope the matrix. List every property in the operator's portfolio. For each property, list every regime that applies (tassa di soggiorno comune, taxe de séjour commune, Bettensteuer city, Kurtaxe Kurort, IEET regional with Barcelona recargo if applicable, Balearic ITS, Lisbon or Porto taxa municipal, Amsterdam toeristenbelasting, etc.). For each regime, capture the legal basis, the published rate, the exemption matrix, the cap, the filing portal, the deadline, the VAT treatment, and the G/L account. The output is a one-page-per-country tax matrix.

Days 4 to 7: audit the PMS posting rules. For each property and each regime, verify that the PMS posting rule matches the matrix. Test the posting on a known sample (a 7-night stay with two adults and one child of the exempt age, a 14-night stay that crosses the cap, a business stay in Berlin with the Arbeitgeberbestätigung, a no-show, an OTA pre-collected reservation). Catalogue every miss.

Days 8 to 11: fix the rules. Update the rate tables, the exemption matrices, the cap parameters, and the posting triggers. Re-test against the same samples until every test passes. Document the changes so the next quarterly review starts from a known-good baseline.

Days 12 to 14: audit the G/L mappings. For each regime, confirm the posting code lands on the dedicated tax-payable G/L account, not on a revenue account. If revenue mis-allocation is found, work with the controller to reclassify historical entries and re-run the affected period closes.

Days 15 to 17: build the reconciliation cadence. Stand up a monthly reconciliation step that pulls the G/L balance, the PMS report, and the regulator's pre-fill (where available), compares the three, and surfaces any difference. The first run usually finds something; fix it. The fifth run usually finds nothing, which is the goal.

Days 18 to 19: build the archive. Create the per-regime per-year archive folder structure. Backfill the past 12 months of filed returns, regulator acknowledgements, bank-statement lines, G/L extracts, and PMS posting reports. The act of backfilling often surfaces a missing acknowledgement or a discrepancy that nobody caught at the time.

Days 20 to 21: handover and calendar. Plot the next 12 months of filing deadlines on the operator's accounting calendar. Brief the controller, the front desk lead, and the night auditor on the rule changes and the new cadence. Schedule the next quarterly review for 90 days out.

Total clerical effort over the 21 days: roughly 50 to 70 hours for the operations-minded person, plus 15 to 25 hours each from the front-desk lead and the controller. Hotels that run this clean reduce their tourist-tax fine exposure by an order of magnitude and close the next audit in under a day.

Where Prostay Fits, Briefly and Honestly

I write for Prostay, so this section is unavoidable; let me be honest about it. Prostay's PMS captures the tourist tax at booking or check-in using a per-property regime selector and a per-regime rate table that ships pre-loaded for the major Italian, French, German, Spanish, Portuguese, Greek, Austrian, Belgian, and Dutch regimes. The exemption matrix runs off the date-of-birth field on the registration record (already captured for police-reporting compliance, see our earlier piece on guest registration and police reporting). Cancellation reverses the line cleanly. The night-audit cycle pushes a posting line into a dedicated short-term liability account in the integrated accounting system, with bank reconciliation at month-end. None of that is unique to Prostay; Mews, Cloudbeds, Apaleo, Profitroom and several regional vendors run a similar rail.

The argument for Prostay specifically is that the rail comes pre-built across every major EU regime (some vendors only cover the home market), the channel manager flags OTA-collected reservations correctly so the PMS does not double-post, and the accounting bridge runs the reconciliation against the bank statement automatically rather than by spreadsheet. The combination matters when a property runs three or more regimes simultaneously, which is the case for most multi-property groups in Spain, Germany, and Italy. If you want the detail, the Prostay PMS overview walks through the posting and reporting modules. If you want help running the 21-day plan with our team on a live property, book a demo and we will work through the regimes that apply to your portfolio without trying to upsell a separate compliance retainer.

Frequently Asked Questions

Five questions independent hoteliers ask most often about European tourist-tax compliance, answered against the published rules rather than the trade-press summary.