Why the PDF Invoice Is Quietly Being Outlawed

For thirty years the corporate invoice has been a PDF on an email. A guest from a company checks out, the front desk prints or emails a branded invoice, the company's accounts payable team types the numbers into their system, and everyone moves on. That workflow is ending, country by country, on a fixed legal timetable, and most independent hotels have not noticed because the change arrives dressed as a tax-administration project rather than a hotel one. Across the EU, structured e-invoicing is becoming mandatory for business-to-business transactions, which means the invoice you send a corporate account, a travel agency, a tour operator, or a conference organiser has to be a machine-readable data file routed through an approved channel, not an attachment. The systems that hold the data behind that invoice, the folio in your PMS and the ledger in your hotel accounting software, are exactly the systems that now have to speak a structured invoice format and connect to a government or partner platform.

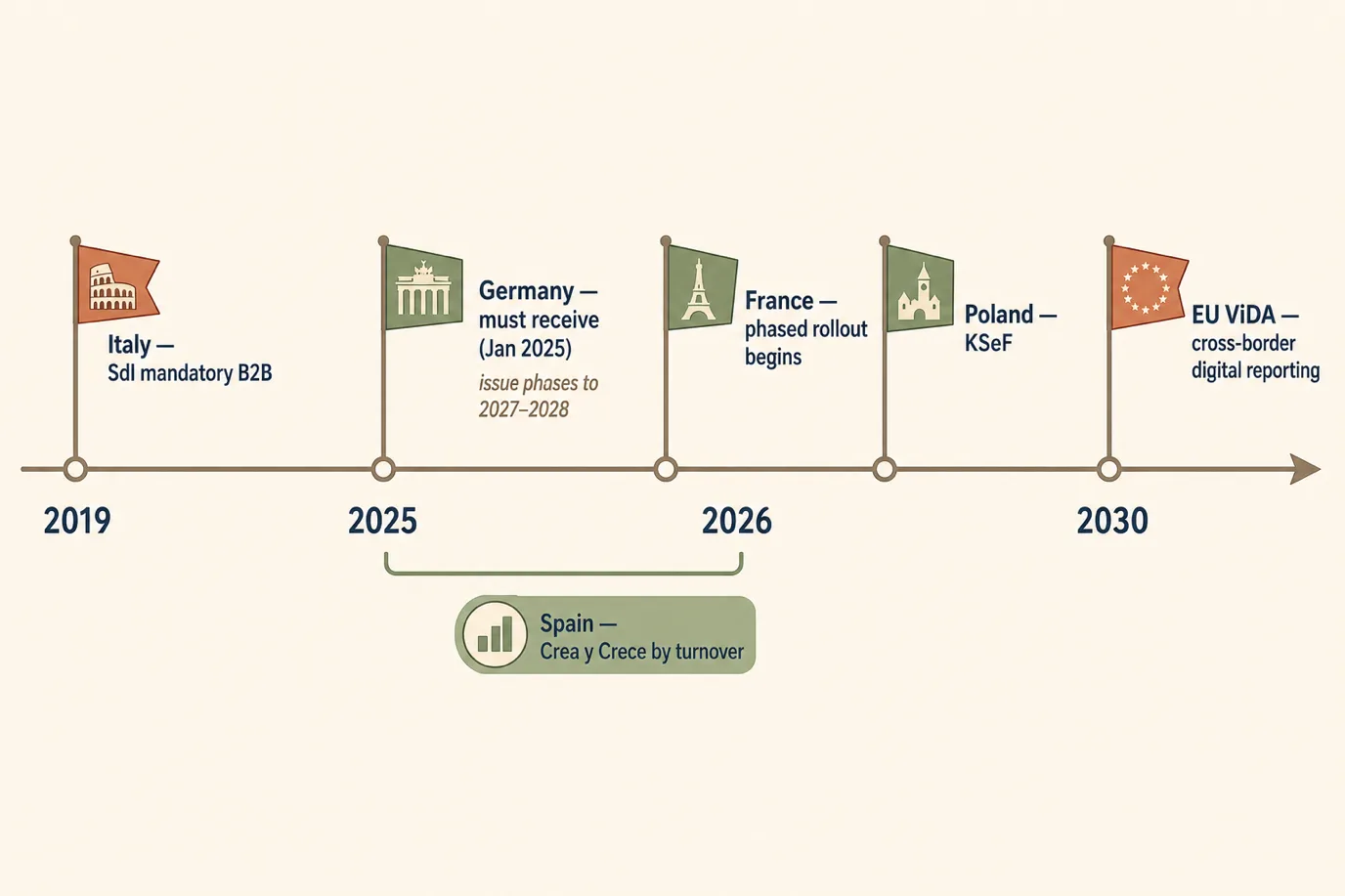

This is not a distant proposal. Italy has required B2B e-invoicing since 2019 and tightened it since. Germany's first obligation landed on 1 January 2025. France begins its phased rollout in 2026, Poland's KSeF mandate arrives in 2026, and Spain is close behind. The invoice data originates in the property management system that runs your folio, so if that system can only print a PDF, you are about to spend staff hours re-keying every corporate invoice into a separate portal by hand. This article is the honest 2026 picture for an independent operator: what e-invoicing actually is, the two regulatory models, which of your invoices are caught, the specific formats per country, the go-live dates, what breaks in a hotel's workflow, and a 30-day plan to get ready without hiring a tax-technology consultant.

I write for Prostay, and our team has spent the last two years connecting hotel folios to the Italian SdI, the French and German exchange routes, and the Spanish reporting systems, so the formats, deadlines, and failure modes below come from the published legislation, the technical specifications each tax authority issues, and the actual integration work on live properties. The deadlines move, occasionally slip, and differ by company size within each country, so treat the dates as the current published position and confirm your specific obligation with your local accountant. What does not move is the direction: the paper-and-PDF era of the B2B invoice is closing, and the hotels that prepare the data layer now will barely notice the switch.

What E-Invoicing Actually Means, and Why a PDF Does Not Count

The word "e-invoice" has been used loosely for years to mean any invoice that arrived electronically. The legal definition is much narrower, and the gap between the loose meaning and the legal one is where hotels get caught. Under the EU framework, an e-invoice is an invoice that has been issued, transmitted, and received in a structured electronic format that allows it to be processed automatically and electronically. The reference point is the European semantic standard EN 16931, which defines the data model an invoice must carry.

A PDF fails this test. A PDF is a picture of an invoice; a human can read it, but a computer cannot reliably extract the supplier VAT number, the line items, the tax rates, and the totals without optical character recognition and a lot of error-prone guessing. A structured e-invoice carries those fields as labelled data (in XML, typically) so the receiving system posts it to the ledger with no retyping. There is a useful middle category, the hybrid invoice, which wraps a human-readable PDF around an embedded XML payload; Factur-X (France) and ZUGFeRD (Germany) are the well-known hybrids, and they satisfy the structured requirement because the machine reads the embedded XML while the person reads the PDF layer.

Two consequences follow for a hotel. First, "we already email invoices as PDFs" is not compliance; it is precisely the practice the mandates are designed to replace. Second, the obligation is usually two-sided and the two sides arrive on different dates. The duty to be able to receive a structured e-invoice almost always lands first and on everyone, because a tax authority cannot mandate issuing without ensuring buyers can accept. The duty to issue structured e-invoices phases in afterward, often by company size. A hotel that books a single corporate event a month still needs, at minimum, to be able to receive structured invoices from suppliers, and will soon need to issue them to that corporate client.

One more clarification that saves confusion later. E-invoicing (the structured invoice between supplier and buyer) is related to, but distinct from, e-reporting (sending transaction or payment data to the tax authority). France's reform, for example, pairs an e-invoicing obligation for domestic B2B with an e-reporting obligation for B2C sales and cross-border transactions, so a hotel selling leisure stays to consumers is not exempt from the reform just because those sales are not B2B e-invoices; the data still has to be reported. Keep the two ideas separate when you read your country's rules.

Two Models: Clearance and Post-Audit Exchange

Behind the formats sits a more important architectural choice each country makes: how the tax authority sees your invoice. There are two models, and knowing which one applies to you tells you more about the operational change than any format name.

The post-audit model is the historical European default. You issue the invoice, send it straight to your customer, and the tax authority only inspects it later, if and when it audits you. Compliance is about keeping correct records and being able to produce them on request. This is the world most hotels still live in, and it is the world that is closing.

The clearance model, sometimes called continuous transaction controls, inserts the tax administration into the flow. The invoice passes through a government platform or an accredited intermediary that validates it (checks the VAT number, the format, the mandatory fields) and registers it, frequently in near real time, before or as it reaches the buyer. Italy's Sistema di Interscambio is the clean example: an Italian invoice does not go directly to the customer at all; it goes to the SdI, which validates it and forwards it. The buyer receives the invoice from the government system, not from you.

France's 2026 reform is a hybrid worth understanding because several countries are copying its shape. Invoices flow through certified private platforms (the plateformes de dématérialisation partenaires, or PDPs) rather than only a single state portal, and those platforms transmit invoice, transaction, and payment data to the administration. It is clearance-style control delivered through a regulated market of intermediaries rather than one monolithic government pipe. Spain's system for the Crea y Crece law leans the same way, with a public solution alongside private platforms.

Why this matters to a hotel: in a clearance country, you cannot quietly fix a mistake by sending a corrected PDF. A wrong invoice has been registered with the tax authority the moment it cleared, so corrections happen through formal credit notes that also clear the platform. The discipline the model demands, correct data the first time, a real channel to transmit it, and a proper correction process, is exactly what a manual PDF workflow lacks. The hotels that struggle in 2026 and 2027 will be the ones that treated the invoice as a document to be typed rather than data to be generated correctly at source.

Which Hotel Invoices Are In Scope

Not every line a hotel issues is caught, and knowing the boundary stops you from either panicking or ignoring the rule. The mandates bite hardest on business-to-business invoices between parties established in the same country. Walk through the hotel's revenue and the picture gets concrete.

Clearly in scope: invoices to a domestic company for a corporate stay, a negotiated corporate rate, or a billed-back room; invoices to a domestic travel agency or tour operator under a contracted allotment; invoices to a domestic event or MICE client for a conference, a banquet, or a block of rooms; invoices to another business for meeting-room hire, catering, or a supplier arrangement. These are the bread-and-butter B2B documents the mandate targets, and for a city hotel with a strong corporate and events mix they can be a large share of issued invoices.

Treated differently, but not ignored: business-to-consumer invoices for ordinary leisure guests. Pure B2C invoices are generally outside the structured B2B e-invoicing duty in the first waves, but several reforms (France most clearly) require e-reporting of those B2C transactions to the tax authority, and some countries are moving B2C into scope over time. So the leisure folio is not a safe harbour you can build a process around; it is the part of the rule most likely to expand.

Cross-border is its own story: an invoice to a company in another EU member state, or to a guest from outside the EU, sits under different rules today and is the focus of the ViDA reforms heading toward the end of the decade. For now, a hotel's domestic B2B invoices are the urgent part; cross-border B2B is the part to watch.

The practical reading: count how many invoices you issue each month to other businesses in your own country. If the answer is more than a handful, e-invoicing is an operational change you have to plan, not a tax footnote. A purely leisure beach property with almost no corporate billing has more time than a city-centre conference hotel, but both will be in scope before the decade is out.

The Formats You Will Actually Send

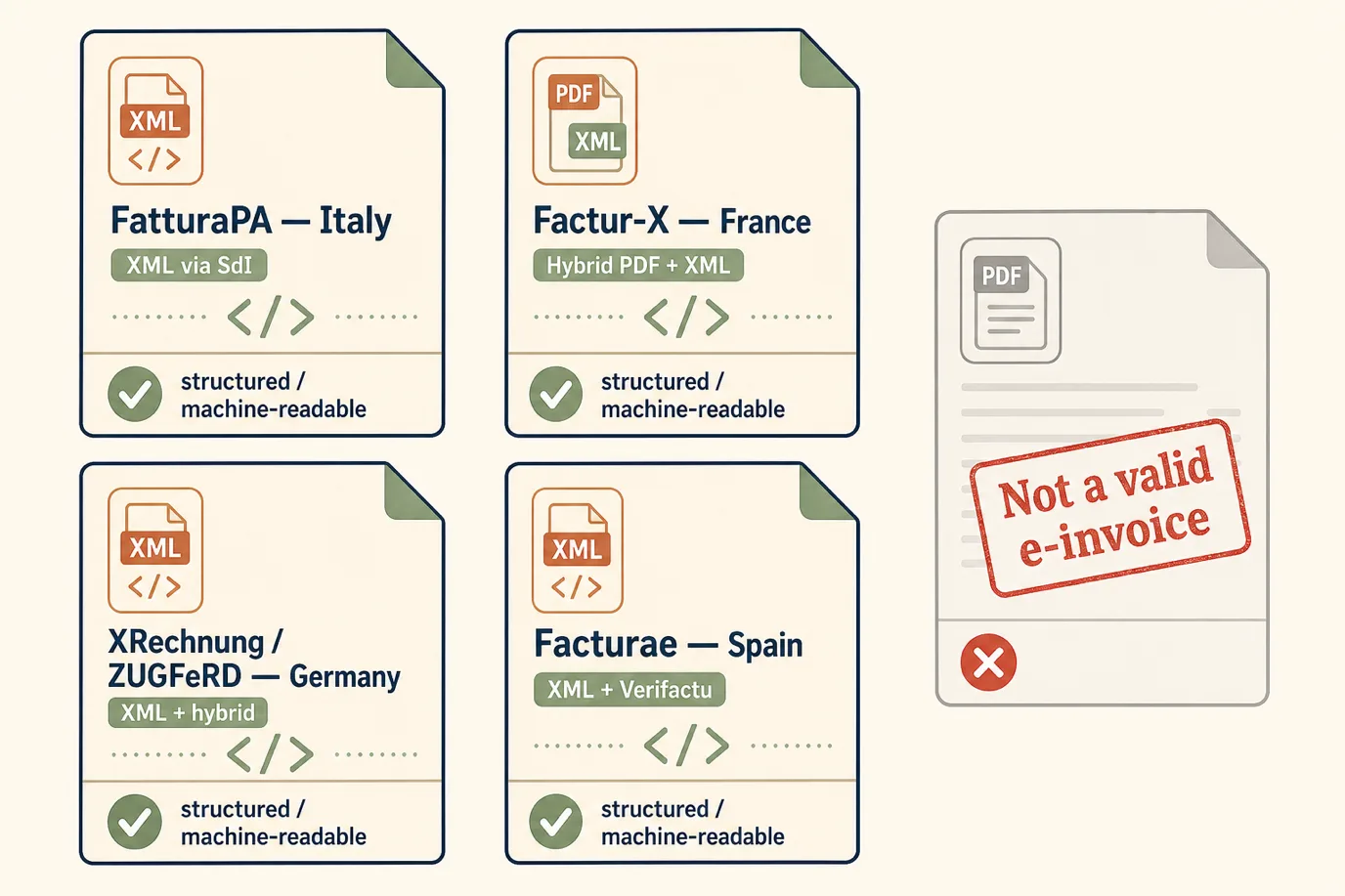

Each country built its mandate on the same EN 16931 semantic core, then chose its own syntax and channel on top. You do not need to read the XML, but you do need to know which format your property must produce, because that determines what you ask your PMS and accounting vendors to support. Here are the four that matter most for hotels operating in the largest EU markets.

Italy: FatturaPA and the SdI

Italy is the most mature regime in Europe and the one every other country studied. The format is FatturaPA, an XML structure, and it is mandatory for almost all VAT-registered businesses for both B2G and B2B since 2019, extended over time to cover small flat-rate taxpayers as well. Every invoice routes through the Sistema di Interscambio (SdI), the state clearing platform, which validates the file and delivers it to the recipient. There is no separate step of emailing the customer; the SdI is the channel. For a hotel, the operational reality is that the PMS or accounting system must generate valid FatturaPA XML, transmit it to the SdI through an accredited intermediary or direct channel, handle the SdI's acceptance or rejection notices, and store the outcome. Rejections are common on the first attempt and usually come from a malformed VAT or fiscal code, a missing mandatory field, or a wrong document type code.

France: Factur-X, PDPs, and the PPF

France's reform is the one to understand in detail because it is large, imminent, and architecturally influential. The default format is Factur-X, a hybrid that embeds EN 16931 XML inside a readable PDF/A-3, which is friendly to a hotel because the human-facing document still looks like an invoice. Transmission runs through certified partner platforms (PDPs), with a public invoicing portal (the Portail Public de Facturation, built on Chorus Pro foundations) playing a directory and reporting role. The French rollout pairs e-invoicing for domestic B2B with e-reporting for B2C and cross-border. Timing is phased by company size: the obligation to receive applies broadly from the first wave, while the obligation to issue starts with large and mid-sized companies and reaches the smallest businesses later. A French hotel needs a PDP relationship (often provided through its accounting or e-invoicing software) and a PMS that can hand over clean structured invoice data.

Germany: XRechnung and ZUGFeRD

Germany's Wachstumschancengesetz introduced a domestic B2B e-invoicing obligation that started on 1 January 2025. The first stage is the receive obligation: from that date, every German business must be able to accept a structured e-invoice. The duty to issue phases in afterward, with thresholds based on turnover running through 2027 and 2028. The accepted formats are XRechnung (a pure XML format originally built for public-sector invoicing) and ZUGFeRD (a hybrid that, like Factur-X with which it is aligned, embeds XML in a PDF). Germany did not, in this phase, build a single central clearance platform on the Italian model; invoices are exchanged directly between businesses in the mandated format, with central reporting elements expected to follow in line with the EU ViDA timeline. For a German hotel, the near-term must-have is the ability to receive and read XRechnung and ZUGFeRD now, and to issue them as the size thresholds reach the property.

Spain: Facturae, Verifactu, and Crea y Crece

Spain has two overlapping strands that hotels confuse. The Crea y Crece law introduces mandatory B2B e-invoicing, phased by company turnover, using the Facturae XML format alongside other EN 16931-compatible formats, transmitted through a public solution or private platforms. Separately, the Verifactu rules (under the anti-fraud framework) govern the billing software itself, requiring certified, tamper-evident systems that can generate the required records and, optionally, report them to the tax agency in real time. The two strands answer different questions: Crea y Crece is about the invoice format and channel between businesses, Verifactu is about the integrity of the software that produces invoices. A Spanish hotel needs billing software that is Verifactu-compliant and capable of issuing Facturae for its B2B invoices, which in practice means using a maintained, certified PMS or accounting platform rather than a spreadsheet or an ad-hoc template.

Go-Live Dates and What Changes When

Dates are the part operators most want and the part most likely to shift, because governments routinely defer e-invoicing deadlines when the ecosystem is not ready (France has already moved its dates once). Treat the following as the current published shape rather than gospel, and confirm your exact obligation with your accountant. The pattern across countries is consistent: the duty to receive comes first and applies broadly, then the duty to issue phases in by company size.

Italy is already fully live and has been since 2019, later extended to flat-rate (forfettario) small taxpayers. If you operate in Italy, this is not a future project; it is current operations, and the only question is whether your stack handles SdI cleanly.

Germany began on 1 January 2025 with the obligation for every business to be able to receive XRechnung and ZUGFeRD. The obligation to issue phases in by turnover, with larger firms first and the long tail of small businesses reaching the mandate through 2027 and into 2028. A German hotel should already be able to receive; issuing readiness is the next milestone.

France begins its phased rollout in 2026. The receive obligation applies broadly from the first wave, and the obligation to issue starts with large and mid-sized enterprises before reaching small businesses in the following phase. French hotels should be lining up a PDP and a PMS-to-platform data path now.

Poland brings its KSeF national e-invoicing system into mandatory force in 2026 after an earlier deferral, on a clearance model similar in spirit to Italy's. Spain phases the Crea y Crece B2B mandate by turnover across 2025 and 2026, with the Verifactu software rules on their own track. Other member states (Belgium, with a 2026 B2B mandate, and several more) are following, which is why a portfolio operator should plan for the whole map rather than one country.

ViDA and the 2030 Cross-Border Horizon

The national mandates are stage one. Stage two is VAT in the Digital Age (ViDA), the EU package agreed in 2025 that sets a common direction for digital reporting and e-invoicing across the union, with the cross-border digital reporting requirements targeted toward the end of the decade (around 2030). ViDA matters to a hotel for two reasons even though its headline dates are years away.

First, it removes some of the friction that made national mandates awkward. Under the older VAT rules a member state needed a special derogation to force domestic e-invoicing, and it could not require it without giving businesses an opt-out; ViDA changes that footing so countries can mandate e-invoicing as the default. That is part of why the national clocks are all ticking now. Second, ViDA points toward a harmonised, EN 16931-based structured invoice for intra-EU B2B transactions with near real-time digital reporting, which means the cross-border invoices that are messy today (a German guest's company billed by a French hotel, say) will eventually run on the same structured rails as domestic ones.

The practical takeaway is not to chase the 2030 detail now. It is that every euro you spend getting a structured, automated invoicing capability working for your domestic mandate is spent on the same capability ViDA will extend cross-border later. There is no separate ViDA project for a well-prepared hotel; there is the data layer you build now and a wider scope applied to it later.

What Breaks in a Hotel's Invoicing Workflow

The mandate looks like a tax change but it lands as an operations change, and it breaks specific, predictable things in how a hotel bills. These are the failure points our integration work surfaces most often.

The PDF export dead end. A PMS that can only produce a PDF invoice forces a manual rekey into a separate e-invoicing portal for every B2B document. That is slow, it introduces transcription errors that get registered with the tax authority in a clearance country, and it does not scale through a busy conference month. This is the single most common and most damaging gap.

Dirty customer master data. A structured invoice demands a valid VAT identification number, the correct legal entity name, and in some countries a specific routing identifier (Italy's codice destinatario or a PEC address, France's SIREN-based identifiers). Hotels that captured corporate guests with a free-text company name and no VAT number now find half their B2B invoices reject on the first clearance attempt. The fix starts at the booking and check-in stage, capturing clean billing identity, not at the invoice stage.

Credit notes and corrections. In a post-audit world a mistake was fixed by reissuing a corrected PDF. In a clearance world the wrong invoice is already registered, so corrections must run through formal structured credit notes that also clear the platform. Hotels without a clean credit-note process create reconciliation tangles that surface at the VAT return.

The OTA and channel overlap. Operators get confused about who issues what. The OTA invoices the hotel for commission (the OTA's obligation); the hotel invoices the corporate or agency client for the stay (the hotel's obligation). Mixing these up, or assuming the OTA "handles invoicing," leaves the hotel's own B2B invoices non-compliant. The hotel is the supplier of the accommodation and owns that invoice.

Deposits, proformas, and timing. A proforma or a deposit request is not a tax invoice, and issuing structured invoices at the wrong moment (at booking rather than at supply, or for a deposit that is later netted off) creates mismatches. The PMS posting logic has to distinguish a proforma from the final tax invoice and issue the structured document at the legally correct point.

How to Set Up Your PMS and Accounting System

The whole compliance question reduces to one architectural goal: the invoice should be generated as correct structured data at the point of supply and transmitted through the right channel automatically, with no human retyping. Getting there has a handful of concrete elements.

Start with where the invoice data is born. The folio in the PMS holds the room charges, the taxes, the extras, and (if captured properly) the customer's billing identity. The PMS therefore has to do two things: capture clean B2B billing data at booking and check-in (legal name, VAT number, routing identifier), and expose the completed invoice as structured data rather than only a printed PDF. If your PMS cannot do the second, no amount of downstream tooling fixes the manual-rekey problem cleanly.

Then decide where the formatting and transmission happen. There are two common architectures. In the first, the PMS hands the structured invoice data to integrated accounting software that formats it into FatturaPA, Factur-X, XRechnung, or Facturae and transmits it through the SdI, a PDP, or the relevant exchange. In the second, the PMS connects to a specialist e-invoicing service (an accredited intermediary or PDP) directly. Either works; what matters is that the path from folio to cleared invoice is automatic and monitored, so a rejection from the platform surfaces as an alert someone actions, not a silent failure discovered at the VAT return.

Build the validation in early. The systems that cope well validate the customer's VAT number and mandatory fields at the moment the corporate booking is taken, not at checkout when the guest is standing at the desk. A real-time VAT-number check (VIES for cross-border, national registers domestically) at booking turns a checkout-time rejection into a booking-time correction. Map your document types too: proforma, deposit request, final tax invoice, and credit note are distinct, and the PMS must issue the structured tax invoice only at the legally correct point.

Finally, test against the real platforms in a sandbox before go-live. Every mature system (the SdI, the French PDPs, the German exchange routes) offers a test environment. Run a corporate stay, a MICE block, a deposit-then-final sequence, and a correction through the sandbox, and confirm each clears. The first run almost always surfaces a data-quality issue; better it surfaces in the sandbox than in a registered, rejected invoice.

Archiving, Integrity, and the Audit Trail

The retention obligation itself is not new. Most EU countries require invoices to be kept for somewhere between 6 and 11 years (10 years is common in Germany, France, and Italy). What e-invoicing changes is the nature of what you keep and the integrity you must be able to prove.

Because the compliant invoice is a structured data file, the thing you must retain is the original file (the XML, or the hybrid PDF/A-3 with its embedded XML), not a re-printed PDF that happens to show the same numbers. Alongside it you should keep any digital signature, the platform's acceptance acknowledgement (the SdI's ricevuta, the PDP's confirmation), and enough metadata to tie the invoice to the booking and the payment. The point of the archive is that, years later in an audit, you can produce the exact file that cleared, demonstrate it has not been altered, and still open it in its original format.

The practical pattern that holds up: let the accounting platform or a certified archiving service hold the originals under a guaranteed-integrity regime, rather than dropping copies into a shared drive where no one can attest to what changed or when. A folder of PDFs on a server is not an e-invoice archive, and an auditor in 2031 will not accept it as one. If your provider offers compliant archiving as part of the service, use it; if not, that is a gap to close before, not after, the mandate bites.

A 30-Day E-Invoicing Readiness Plan

A 30-day plan to take a typical independent from "we email PDFs" to "we generate and transmit compliant structured invoices." One finance-minded person can run it, pulling in the PMS and accounting vendors for the technical pieces.

Days 1 to 4: scope your obligation. Confirm, with your accountant, which mandate applies in each country you operate in, the current go-live date for your company size, and whether your near-term duty is to receive, to issue, or both. Count your monthly B2B invoices by type (corporate, agency, MICE, supplier) so you know the volume and the stakes.

Days 5 to 9: audit your data. Pull a sample of recent corporate and agency invoices and check the billing master data: legal entity name, VAT number, country routing identifier. Quantify how many would reject on a structured-format validation today. This number is usually the real project, and it is a front-desk and reservations data-capture fix as much as a finance one.

Days 10 to 16: pin down the systems. Ask your PMS vendor, in writing, whether it generates structured invoice data (not just PDF) for your country's format, and ask your accounting or e-invoicing vendor how it transmits to the SdI, a PDP, or the relevant exchange, and whether it provides compliant archiving. Where a vendor cannot answer, log it as a risk and a procurement decision.

Days 17 to 22: fix data capture at source. Update the booking and check-in workflow so corporate billing identity (legal name, VAT number, routing code) is captured and validated when the reservation is made, not improvised at checkout. Clean the existing corporate-account records you bill repeatedly.

Days 23 to 27: test in the sandbox. Run a corporate stay, a MICE block, a deposit-then-final invoice sequence, and a credit-note correction through the platform's test environment. Confirm each clears and that rejections surface as actionable alerts. Iterate until the common cases pass cleanly.

Days 28 to 30: document and brief. Write a one-page procedure covering which invoices go through the structured channel, who monitors rejections, how corrections are issued, and where originals are archived. Brief the front desk, reservations, and the night auditor on the data-capture change, because the compliance outcome is decided at booking, not at billing. Put the next-country go-live dates on the calendar if you operate in more than one.

Total effort over the 30 days: roughly 20 to 35 hours for the finance lead and a focused block from the PMS and accounting vendors, concentrated in the data-cleanup and sandbox-testing weeks. The properties that run this calmly are the ones that treated the invoice as data generated at source, not a document typed at the end.

Where Prostay Fits, Briefly and Honestly

I write for Prostay, so this section is unavoidable; let me be straight about it. Prostay's PMS captures corporate and agency billing identity (legal name, VAT number, routing identifier) at the booking and check-in stage, validates it, and generates the invoice as structured data rather than only a printed PDF. That structured invoice flows into the integrated accounting system, which formats it for the relevant national standard (FatturaPA, Factur-X, XRechnung, Facturae) and transmits it through the SdI, a French PDP, the German exchange route, or the Spanish channel, with rejections surfaced as alerts and originals archived under a compliant regime. None of that is unique to Prostay; Mews, Cloudbeds, and several regional vendors have built or partnered for the same capability, and any maintained, certified platform can meet the mandate.

The argument for Prostay specifically is that the folio, the invoice generation, and the accounting handover come from one team that tests them together against each national platform, so you are not bolting a separate e-invoicing portal onto a PMS that can only print PDFs and rekeying between the two. That single data path from folio to cleared invoice is the whole game, and it is what removes the manual step the mandate is designed to kill. If you want the detail on the folio and billing side, the Prostay PMS overview walks through it, and if you would rather have our team map your specific country obligations against your current stack, book a demo and we will work through the invoices you actually issue rather than sell you a separate compliance module.

Frequently Asked Questions

Five questions independent hoteliers ask most often about mandatory e-invoicing, answered against the published legislation and the technical standards rather than the trade-press summary.