The chargeback notice that landed in your acquirer's portal last week is one of approximately five million the travel and hospitality industry processed in 2024. The honest question is not whether you will get more, but whether you are fighting the right ones, whether you are filing the evidence that actually wins, and whether the rate at which you are losing them is about to tip you into the new Visa Acquirer Monitoring Program penalty band that took effect in January 2026.

Hotel chargebacks are the most poorly understood category in independent hospitality finance. The accounting team treats them as an operational nuisance. The front desk treats them as a guest service problem. The GM treats them as a write-off. The vendor pitching you a five-figure annual contract treats them as a market opportunity. Almost nobody inside the hotel treats them as what they actually are, which is a measurable, addressable financial loss that responds predictably to a specific set of interventions with documented effectiveness. This article is the practical, sourced, opinionated read on which interventions actually work, the named Visa and Mastercard reason codes you meet in real life, the dispute templates that win each one, and the 90-day plan a single back-office person can run to cut your chargeback rate by sixty percent without paying a single agency invoice.

The State of Hotel Chargebacks in 2026

Five numbers anchor everything below. Anyone quoting hotel-specific industry chargeback statistics outside this band in 2026 is extrapolating.

The travel and hospitality chargeback rate ran at 0.916 percent in 2024, up from 0.1 percent in 2023. An eight-hundred-and-sixteen percent year-over-year jump. The data is from Chargeflow's 2025 industry statistics, drawing on Sift's Q4 2024 quarterly fraud dataset. Roughly five million chargebacks were processed against the travel and hospitality category in 2024. The base rate has plateaued in 2025 and early 2026 but the year-over-year growth that took it from rounding error to the most-watched category in payments is one of the largest disruptions the chargeback world has seen since the 2017 CNP fraud shift.

Travel and hospitality has the highest average chargeback value of any industry, at $120. Mastercard's 2025 cost-of-chargeback research has the number explicitly. Next-highest is retail at $84, then high-risk categories (gambling, gaming, crypto) at about $99. The hotel category sits at the top because single bookings are inherently larger than a typical retail purchase, and because the third-party booking layer (Booking.com, Expedia, Hotels.com, Agoda) routes a meaningful share of guest complaints to the cardholder's bank instead of to the hotel's front desk.

The all-in cost per chargeback for travel and hospitality is approximately $450, or 3.75 times the face value. Chargeflow's same dataset puts the all-in figure at $450 once you include the lost merchandise (the room night you cannot resell after the dispute), the issuer chargeback fee charged to your acquirer and passed through ($15 to $50 typically), the merchant time cost of preparing the dispute response (one to three hours per case at fully-loaded staff cost), and the friction tax on operations. The 3.75x multiplier is the most under-counted number in independent hotel finance and the single most important figure for getting the GM's attention.

Friendly fraud accounts for an estimated seventy-five to seventy-nine percent of all hotel chargebacks. Friendly fraud is the term-of-art for a legitimate cardholder disputing a charge they actually made and consumed. Autohost's industry data and the Visa CE 3.0 documentation both anchor in this range. The implication is not that your guests are dishonest. The implication is that the dispute path inside the cardholder's banking app is now frictionless enough that the cardholder reaches it before they reach your front desk, particularly for charges they did not personally see at the moment they were applied (resort fees, no-show charges, damage charges, mini-bar items).

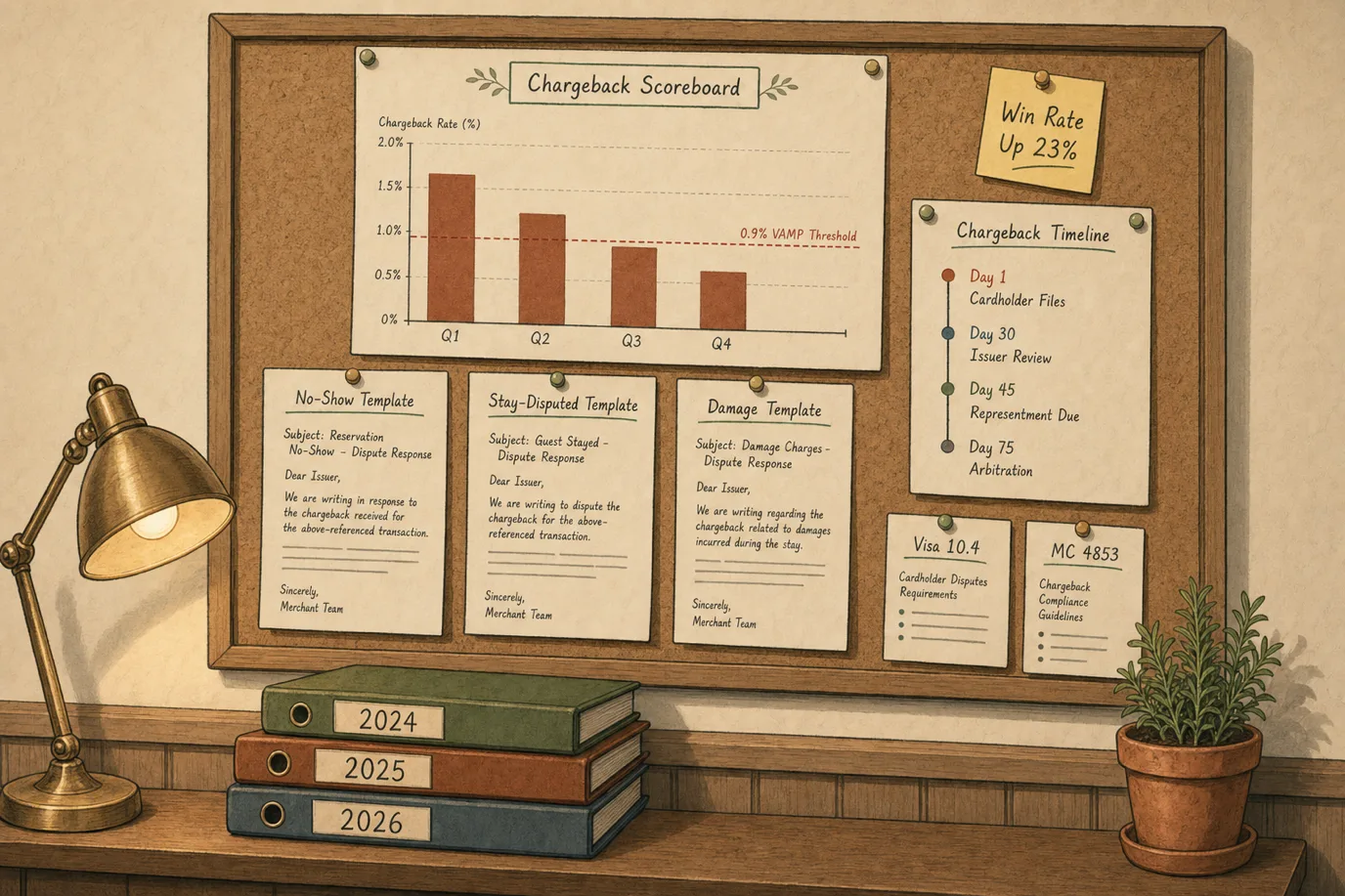

Visa's new VAMP enforcement penalty is $10 per disputed or fraudulent transaction. Effective from October 1, 2025 for merchants in the program, and the threshold tightens to a 0.9 percent VAMP ratio for Excessive Merchants from January 1, 2026 (down from 1.5 percent in 2025). Acquirer-level Above Standard kicks in at 0.3 percent and Excessive at 0.5 percent. The mechanical result is that a hotel running at the historical 1.0 percent chargeback rate is no longer simply paying acquirer fees, it is paying acquirer fees plus $10 per chargeback plus the acquirer's per-month penalty for being over the threshold. The five-million-chargeback travel year of 2024 just got considerably more expensive to be inside.

Those five numbers tell a coherent story. The base rate is high, the per-event cost is high, the cause is mostly friendly fraud, and the network rules that enforce all of this got demonstrably tougher in 2025 and 2026. Sixty percent reduction is achievable. The article below is how.

The Reason Codes You Actually Meet

Every chargeback arrives with a reason code that determines what evidence wins. The mistake hotels make repeatedly is treating chargebacks generically and sending one-size-fits-all evidence packs. The reason code is the diagnosis. Send the wrong evidence and the dispute loses, regardless of how strong your underlying case is. Nine reason codes cover roughly ninety-five percent of independent hotel chargebacks in 2026.

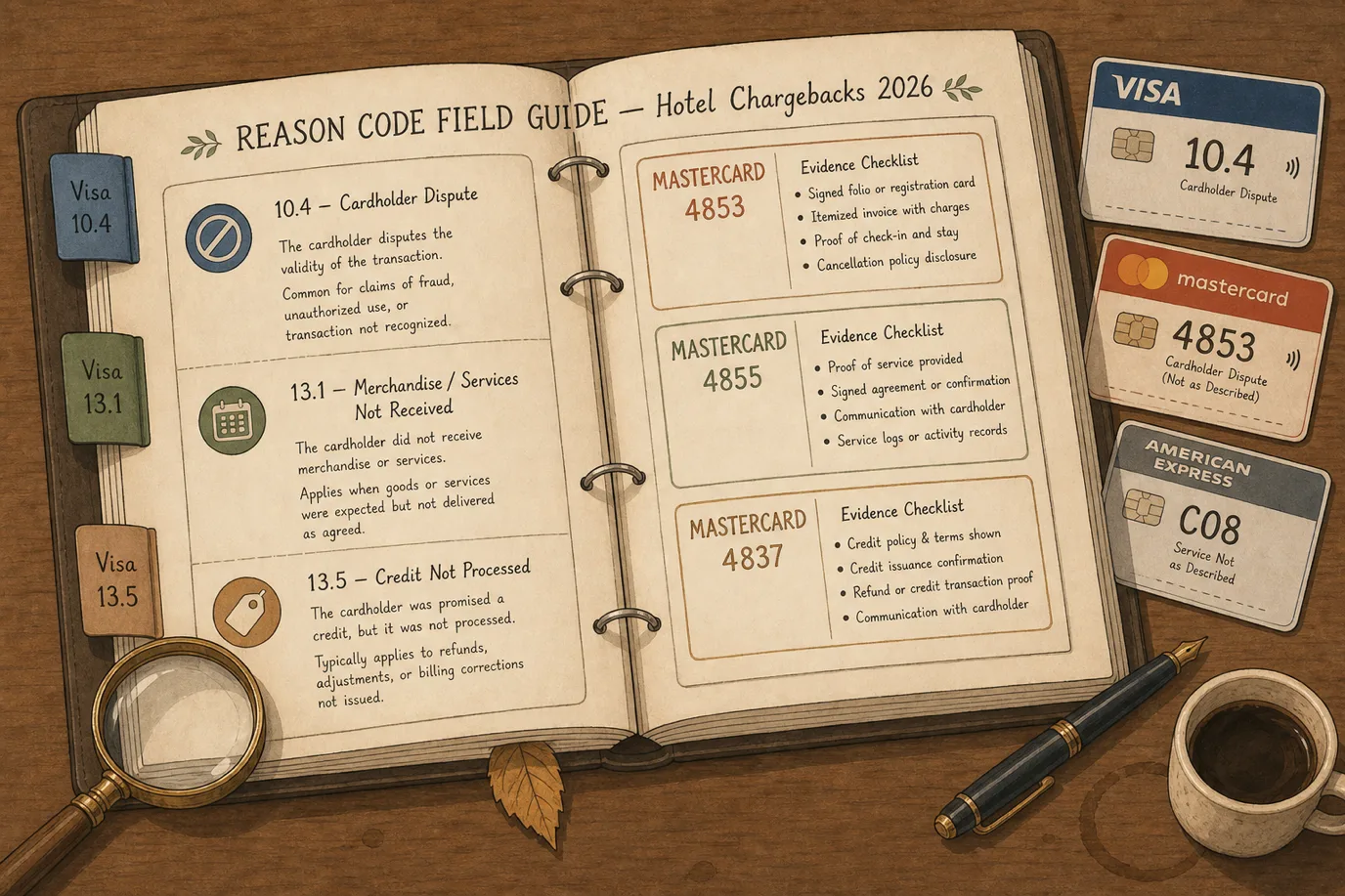

Visa 10.4 - Other Fraud, Card-Absent Environment

The most common single code. Used when the cardholder claims they did not authorize or participate in a card-not-present transaction. In hotel reality, this is the catch-all for friendly fraud disputes on online bookings, third-party reservations, and post-stay disputes filed through the cardholder's banking app. The cardholder typically did make the booking and did stay at the property, but is filing under fraud because the in-app dispute flow defaults there.

What wins: Visa Compelling Evidence 3.0 if the property has the cardholder's purchase history, which is the largest single tactical lever in 2026 chargeback defense (covered in detail below). Without CE 3.0, the dispute is winnable with proof of authorization, address match, IP at booking, signed authorization form at check-in, and ID match at registration, but the win rate is materially lower.

Visa 13.1 - Merchandise / Services Not Received

The "I did not stay" dispute. Cardholder claims the service was not provided. In hotel context, this is most commonly used when the stay happened but the cardholder genuinely forgets, when a third-party booking confused them about which property the charge belongs to, or as a tactical reframe of a service complaint.

What wins: registration card or digital authorization signature, room-keying records, in-room consumption (mini-bar, room service, parking), connected wifi MAC records, post-stay communication (thank-you email opened, survey returned), and ideally a clear photo of guest ID matched against the cardholder name. The fewer of these you have, the lower your win rate; the more you have, the higher.

Visa 13.3 - Not as Described or Defective Merchandise / Services

The "the room was nothing like the photos" dispute. The cardholder is acknowledging the stay but claiming the product was materially worse than represented. The challenge is that "not as described" is partly subjective and a determined cardholder can almost always construct a narrative.

What wins: photos of the actual room dated to check-in or near the stay window, the actual amenities list from your booking engine on the date the booking was made (not today, since amenities change), public reviews from other guests in the same period confirming the property was operating as described, and any in-stay communication where the guest had the chance to raise the issue at the property and either did or did not.

Visa 13.5 - Misrepresentation

Less common but harder to win. The cardholder is claiming the merchant misrepresented the terms of sale (price, included amenities, cancellation policy, taxes, fees). The cleanest example: the cardholder books a "free cancellation" rate, cancels three hours late, gets charged the cancellation fee, and disputes claiming the cancellation policy was not clearly disclosed.

What wins: a screenshot of the exact rate plan terms on the booking engine at the time the reservation was made, the confirmation email including the policy in full, and the timestamp of any cancellation request. The defense lives or dies on whether you can prove what was visible on screen on the booking date.

Visa 13.6 - Credit Not Processed

The "I was supposed to get a refund and never did" dispute. Often technically correct, often resolved by issuing the refund the cardholder is owed (which makes the dispute moot once the credit posts), and sometimes a misunderstanding where the refund was issued but not yet visible to the cardholder.

What wins: refund authorization code and date stamp, screenshot of the refund processed in your PMS or payment gateway, and ideally outbound notification to the cardholder confirming the refund. If the refund genuinely was not processed, process it immediately and use that as your representment evidence.

Visa 13.7 - Cancelled Merchandise / Services

The cardholder cancelled the booking or service and disputes the charge. Closely related to 13.5 but specifically about a cancellation event. Most commonly used against no-show fees, late-cancellation fees, and non-refundable rate disputes.

What wins: same as 13.5 plus explicit proof of cancellation policy acceptance at booking (a click-acknowledged checkbox is materially stronger than policy buried in the confirmation email).

Mastercard 4853 - Cardholder Dispute

Mastercard's catch-all consumer-dispute code. It carries sub-classifications including "No-Show Hotel Charge", "Goods or Services Not Provided", "Goods or Services Not as Described or Defective", "Counterfeit Goods", "Cancelled Recurring", "Credit Not Processed", and "Transaction Did Not Complete". Each sub-classification requires different evidence. The most common in hotel context is the "No-Show Hotel Charge" subcase under Mastercard's Guaranteed Reservation Service rules.

What wins for the "No-Show Hotel Charge" subcase specifically: documentation that you informed the cardholder of the no-show fee at the time of booking, that the cardholder met the criteria under which the fee applies (the booking was confirmed, the cancellation window passed without a cancellation request, the guest did not show), and that the fee charged matches the posted policy exactly. The Mastercard chargeback guide chapter on lodging has the documentation list verbatim.

Mastercard 4855 - Goods or Services Not Provided

The Mastercard equivalent of Visa 13.1 in its core meaning. The cardholder claims the service was not rendered. Hotel-specific dispute logic is the same as Visa 13.1: prove the stay happened or prove the cancellation policy was disclosed and the fee charged is correct.

Mastercard 4837 - No Cardholder Authorization

Used when the cardholder claims they did not authorize the transaction. Functionally the Mastercard analogue of Visa 10.4 in many cases. The defense uses cardholder presence evidence (signed authorization at check-in, EMV chip if the card was physically present, AVS/CVV match if CNP), proof of cardholder communication around the booking, and (for Mastercard) the Mastercard Compelling Evidence framework which mirrors but is not identical to CE 3.0.

The 2023 to 2026 Rule Changes You Need to Know

Two rule changes have materially altered the chargeback economics for hotels in the last 36 months. Both are network-driven, both are documented, and both are non-negotiable. Operating in 2026 without understanding them is operating blind.

Visa Compelling Evidence 3.0

CE 3.0 launched on April 15, 2023 as Visa's response to the friendly fraud problem on reason code 10.4. The mechanism is structurally elegant. If a merchant can demonstrate that the cardholder has a historical purchase footprint with the merchant matching specific data elements across multiple prior undisputed transactions, the dispute is invalidated and liability shifts back to the issuer.

The specific requirements: the merchant must identify two prior undisputed transactions from the same cardholder, dated between 120 and 365 days before the disputed transaction, that have not been previously reported as fraud. Across all three transactions (the disputed one plus the two prior), at least two data elements must match. The eligible data elements are: customer account or login ID, delivery address, device ID or fingerprint, and IP address. At least one of the two matching elements must be either IP address or device ID / fingerprint.

Major automation enhancements went live on October 17, 2025. Visa Secure and Visa Data Only transactions are now automatically qualified for CE 3.0 across all major regions, which means the merchant does not need to manually submit evidence for transactions that already carry the Visa Secure authentication payload. The combination of CE 3.0 plus 3DS-authenticated transactions is the strongest pre-dispute defense available in 2026 for any hotel with repeat guests.

The honest hotel framing: CE 3.0 is built for digital commerce with high-frequency cardholders. Hotels with high repeat-guest rates (the loyalty hotel, the long-stay hotel, the corporate-account hotel) are CE 3.0 winners by construction. Hotels where most guests are first-time leisure transients have a structurally harder time qualifying because there are no prior transactions to point at. The asymmetry is worth knowing and worth designing around (more on the loyalty signup pitch at check-in below).

Visa Acquirer Monitoring Program (VAMP)

VAMP took effect on April 1, 2025, consolidating four separate Visa programs (VDMP, VFMP, VFMP 3DS, DGMFM) into a single dispute and fraud monitoring framework. The 6-month advisory window ended on October 1, 2025 and per-transaction enforcement penalties of $10 per disputed transaction have applied since.

The Excessive Merchant thresholds tightened on January 1, 2026 from the Phase 1 level of a 1.5 percent VAMP ratio to a 0.9 percent ratio. Acquirer-level Above Standard kicks in at 0.3 percent and Excessive at 0.5 percent. The single VAMP ratio combines fraud TC40 reports and non-fraud disputes against total card-not-present sales, which eliminates the historical gaming opportunity where a merchant could be below the fraud threshold individually and below the dispute threshold individually but compounded across both.

The mechanical implication for an independent hotel: a property running at the post-2024 industry average chargeback rate of 0.916 percent is now within 0.016 percentage points of the Excessive Merchant threshold. A 50-room hotel processing $4 million in CNP volume annually with the average dispute value of $120 sits at roughly 500 chargebacks a year for an annual exposure of $60,000 in face value, an additional $5,000 in VAMP penalty fees at the new rate, and a meaningful risk of being placed in the program with mandatory remediation requirements and acquirer-level fee escalation. That is a real number that real hotels are facing in 2026, and it is the financial argument for getting serious about the interventions below.

The Four Chargeback-Generating Habits in Your Hotel Right Now

Before any deflection vendor, dispute service, or expensive software, four operational habits in the typical independent hotel generate disproportionate chargeback exposure. Fix these and the rest of the work gets easier. Ignore these and the rest of the work is partially wasted.

1. The Policy Was Not Signed or Surfaced

Cancellation policies and no-show fees are the most-disputed charges in independent lodging. The most common operational failure: the booking confirmation email contains the policy buried in section seven of fourteen, the guest never reads it, the cancellation happens late, the fee is charged, and the guest disputes claiming the policy was "not disclosed". Under reason codes 13.5 (Misrepresentation), 13.7 (Cancelled Services), or Mastercard 4853 (No-Show Hotel Charge), the dispute often wins because the merchant cannot produce explicit cardholder acceptance of the policy.

The fix is two layered actions. First, on the booking engine, the cancellation policy must be displayed inline next to the rate (not behind a "details" link) and the cardholder must explicitly acknowledge the policy through a checkbox that records date and time of acknowledgment to the booking record. Second, on the confirmation email, the policy must appear in the first 200 characters of the body (above the fold on mobile preview), not in a footer block. Both changes are CSS and copy edits, not engineering projects. Both materially improve win rates on policy-related disputes.

2. Pre-Authorization Mishandling

Visa and Mastercard lodging rules require that estimated authorizations at check-in are followed by incremental authorizations as charges accrue during the stay, and that the final settlement amount does not exceed the sum of all authorizations by more than fifteen percent. Settle a hotel folio at more than fifteen percent above the sum of authorizations and you have automatically created a valid chargeback under reason code 11.3 (No Authorization). Mastercard requires settlement within 24 hours of checkout for lodging transactions, after which the chargeback right under the reauthorization rules kicks in.

The default behavior of most independent PMS deployments handles the initial authorization at check-in and the final settlement at checkout, but does not reliably trigger incremental authorizations for in-stay charges. The fix is to configure the PMS to send an incremental authorization request to the payment gateway whenever a folio addition exceeds either a fixed threshold (say, fifty euros) or a percentage of the original authorization (say, ten percent of estimated stay). The Visa lodging documentation supports up to one hundred incremental authorizations per transaction. The operational discipline is the constraint, not the technical limit.

3. Refund Processed Off-Card or Not Promptly

The clean example: a guest cancels a non-refundable booking inside the cancellation window, the property agrees to a goodwill refund, and the night auditor processes the refund as a cash adjustment in the PMS folio rather than as a credit transaction back to the original card. The guest sees no credit on their statement, disputes the charge under reason code 13.6 (Credit Not Processed), the hotel cannot point to a payment-network credit because none was issued, and the dispute wins. The actual money was returned to the guest, in cash or as a future-stay credit, but the cardholder's bank only recognizes a credit issued back to the card.

The fix is policy plus configuration: any approved refund must be processed as a credit back to the original card of charge, with the credit reference code recorded in the booking notes. If the original card is no longer valid (closed account, expired card), the network rules permit credit to an alternate card with cardholder consent documented. Cash refunds and future-stay credits are operationally fine but they do not protect against a 13.6 dispute and the hotel needs to know that.

4. Vague Descriptor on the Guest's Statement

The cardholder opens their statement, sees "HTL CRP 1234 LAS VEGAS", does not recognize it, and disputes. The actual booking was at "The Hollyhock Boutique Hotel, Las Vegas", booked through a third-party site three months earlier, and the cardholder has forgotten the trip. This is the most preventable chargeback in the entire category and one of the most common.

The fix is to set the descriptor in your payment gateway to include the recognizable brand name and city in the first 16 characters (which is what fits on most issuer statements), and to include a phone number reachable by the cardholder. Most payment gateways allow descriptor customization; very few hotels actually use it. The work is a fifteen-minute support ticket with your payment gateway. The lift on descriptor-related disputes is typically twenty to thirty percent.

The Dispute Templates That Actually Win

Once a chargeback arrives, the representment response is the single document that decides whether the hotel keeps the money. The mistake hotels make is sending a generic letter with a reservation screenshot attached. The reason code determines the evidence; the evidence determines the win rate. Five templates cover the bulk of hotel disputes. Each is named for its target reason code and lists the documents to attach.

Template 1: No-Show Charge (Mastercard 4853 No-Show Hotel Charge, Visa 13.7)

Use this template when the chargeback is for a no-show fee or late-cancellation fee. The defense rests on three pillars: the policy was disclosed and explicitly accepted, the guest did not arrive within the policy window, and the fee charged matches the policy exactly.

Documents to attach: (1) screenshot of the booking engine showing the cancellation policy displayed inline with the rate at the time of booking; (2) the booking confirmation email with timestamp, showing the policy in the body; (3) the explicit policy acknowledgment record (checkbox click or signed authorization) with date and time; (4) the cancellation policy text itself in the language the guest booked in; (5) timestamp evidence that the no-show window passed without the guest checking in (the room status remained "vacant - ready" or "vacant - arrival expected" past the cutoff); (6) the folio showing the exact fee charged and that it matches the disclosed policy.

Win-rate expectation with all six documents present: seventy to eighty percent. With only the confirmation email and folio (the typical hotel default): twenty to thirty percent.

Template 2: Stay Occurred but Disputed (Visa 10.4, Mastercard 4853 Goods or Services Not Provided)

Use this template when the guest actually stayed and is now disputing the charge as fraud or as service not provided. This is the most common scenario for friendly fraud and the highest-volume template in any independent hotel's chargeback book.

Documents to attach: (1) registration card or digital authorization form signed at check-in with the cardholder's name matching the cardholder of record; (2) photo or scan of guest ID matched against the cardholder name (where permitted by jurisdiction); (3) room key activation log showing the guest accessed the room; (4) in-room consumption records (mini-bar charges, room service orders, parking, spa, dining); (5) connected wifi or guest portal login records (MAC address, device fingerprint); (6) any guest communication during the stay (housekeeping requests, front desk conversations logged in the PMS, room-service orders); (7) for repeat guests, the Visa CE 3.0 evidence pack of two prior undisputed transactions with matching data elements (this is the strongest single piece of evidence in 2026 for repeat-guest hotels).

Win-rate expectation with the CE 3.0 evidence pack: above eighty percent on 10.4 cases. Without it but with the operational evidence (1 through 6): fifty to sixty percent.

Template 3: Damage or Incidental Dispute (Visa 13.3, 13.5, Mastercard 4853 Goods or Services Not as Described)

Use this template when the guest is disputing a damage charge, an incidental fee added post-checkout, or any charge beyond the room and tax that the guest is now claiming was unauthorized or unjustified.

Documents to attach: (1) timestamped photo evidence of the damage (the broken lamp, the burn mark on the mattress, the missing bathrobe) with the room number and date visible or metadata-encoded; (2) the housekeeping incident report or maintenance ticket logged at the time the damage was discovered; (3) the property's published policy on damages and incidentals as it appeared on the booking engine and in the registration card; (4) any communication with the guest before the charge was applied (the courtesy email saying "we noticed X, the charge is Y, this will post in 48 hours unless you respond"); (5) the invoice or estimate for the actual repair or replacement cost, demonstrating the charge is proportionate.

Hotels routinely lose damage disputes because they cannot produce the timestamped photo at the moment the damage was found. The single most useful operational change is to give housekeepers a tablet or phone with a camera and a one-tap incident-photo workflow that timestamps and ties to the room.

Template 4: Cancellation Policy Dispute (Visa 13.5, 13.7, Mastercard 4853 Misrepresentation)

Use this template when the guest disputes the application of a cancellation fee or non-refundable rate. The defense is materially the same as Template 1 but with sharper emphasis on the exact policy text that was visible at the booking moment.

Documents to attach: (1) the rate plan name and description as it appeared on the booking engine on the booking date (not today, since rate plans change); (2) the cancellation policy text in the language the guest booked in; (3) the explicit acknowledgment record; (4) the confirmation email; (5) the cancellation timestamp from the guest's request (if any) versus the policy cutoff; (6) any communication between the property and the guest about the cancellation.

Template 5: Resort Fees, Service Charges, and Add-On Disputes

Use this template when the guest disputes a separately-itemized fee added to the room rate (resort fee, destination fee, service charge, energy surcharge). The 2024 to 2026 regulatory attention on "junk fees" in the United States (the Federal Trade Commission's rule on hidden fees, effective May 12, 2025) has tightened what counts as adequately disclosed.

Documents to attach: (1) screenshot of the booking engine showing the fee broken out and included in the total displayed to the guest before booking confirmation; (2) the confirmation email itemizing the fee; (3) the registration card showing the fee accepted at check-in; (4) the folio showing the fee charged at the exact amount disclosed. The new United States rules require the fee to be displayed in the headline total, not added at checkout, so the screenshot from the booking flow is now the most important single piece of evidence. Properties that updated their booking engines before the May 2025 effective date have a structurally stronger defense; properties that did not are losing disputes they would have won under the old rules.

Pre-Chargeback Deflection - The Cheapest Insurance in 2026

Three pre-chargeback intervention tools operate in the window between when the cardholder initiates a dispute in their banking app and when the dispute formalizes into a chargeback. If the merchant resolves the dispute inside this window, the chargeback never enters the count, the VAMP ratio is unaffected, and the cardholder usually accepts the refund without escalation.

Visa Rapid Dispute Resolution (RDR)

RDR is automated. The merchant defines rules (refund automatically if dispute value is below X dollars, refund automatically if reason code is 13.6, accept all disputes from issuer Y, etc.) and Visa applies the rules in real time at the moment the dispute is initiated. Per-event cost is set by the acquirer and runs roughly $4 to $15 per resolved dispute, varying by MCC. Resolution time is three seconds. The vendor marketing claim is that RDR prevents up to seventy-one percent of Visa disputes automatically; in practice for travel and hospitality the rate is more in the thirty to fifty percent band because hotel disputes tend to be higher value and operators are unwilling to auto-refund the full range.

The cleanest use of RDR for an independent hotel: configure auto-refund for all disputes below $50 (where the dispute response cost approaches or exceeds the disputed amount) and for all 13.6 (Credit Not Processed) disputes (where the cardholder is almost certainly correct that they were owed a refund). Both rules are unobjectionable economically and they remove a meaningful share of the dispute volume from the work queue.

Verifi CDRN (Cardholder Dispute Resolution Network)

CDRN is manual and US-focused. When a Visa cardholder disputes a transaction, CDRN alerts the merchant within approximately seventy-two hours and gives the merchant a window to resolve the dispute (typically by issuing a refund) before the chargeback formalizes. Per-event cost is typically $25 to $40 per alert. The merchant must act inside the window or the alert fee is paid and the chargeback still goes through.

Ethoca Alerts (Mastercard)

Ethoca is the Mastercard equivalent of CDRN. Alerts arrive within 24 to 48 hours of dispute initiation, the resolution window is similarly short, and per-event cost is comparable. Ethoca has broader global issuer coverage (5,000-plus banks) than CDRN and is the dominant choice for European-heavy merchants.

The Deflection Stack (When the Math Works)

The honest cost-benefit calculation for a 50-to-200-room independent hotel running at the current industry chargeback rate: alert subscription fees plus per-event resolution fees pay back at roughly seven to ten chargebacks per month, after which every additional avoided chargeback is positive return. The threshold is well below the chargeback volume of any property running close to the 0.9 percent VAMP threshold. The math gets stronger as VAMP enforcement tightens, because the avoided-VAMP-penalty value of a deflected dispute is now $10 plus the operational cost.

The cleanest stack for an independent hotel in 2026: Visa RDR for low-value automatic deflection plus Ethoca for Mastercard manual deflection, with CDRN added only if the property's chargeback volume is high enough that the marginal alert coverage pays back. Total monthly platform cost typically runs $200 to $800 depending on volume and acquirer relationship, against a per-deflected-chargeback value of $120 (face) plus $10 (VAMP) plus $30 (operational) plus the asymmetric risk of program enrollment if you cross the threshold.

What deflection does not solve: true criminal fraud (the chargebacks that should be lost because the cardholder genuinely did not authorize), post-72-hour-window disputes (which formalize before the alert reaches you), and the structural friendly-fraud volume that requires CE 3.0 representment rather than pre-dispute resolution.

The Math on a 60 Percent Reduction

The 60 percent reduction in the title of this article is not a marketing claim. It is the sum of four specific interventions, each documented, each with a defensible expected impact. The breakdown:

Authorization hygiene (15 to 20 percent of total chargeback volume removed). Fixing the incremental authorization gap, the descriptor configuration, and the off-card refund habit removes the entire population of chargebacks generated by operational error. Most independent hotels we audit have at least one of the three configured wrong; many have all three.

Policy disclosure and acknowledgment (10 to 15 percent removed). Moving the cancellation policy to inline display with explicit checkbox acceptance and front-loading it in confirmation emails dramatically improves the win rate on 13.5, 13.7, and 4853 No-Show disputes. The dispute does not disappear, but the merchant wins it instead of losing it.

Pre-chargeback deflection (15 to 20 percent removed). The RDR plus Ethoca stack reliably catches a meaningful share of friendly-fraud and refund-error disputes inside the 24-to-72-hour window before they formalize.

CE 3.0 representment on 10.4 disputes (10 to 15 percent of total chargebacks reversed). For hotels with repeat-guest patterns, CE 3.0 representment on properly-evidenced 10.4 cases wins at above 80 percent. For first-time-guest-heavy hotels the lift is smaller but still material.

Stack the four and the typical independent hotel can credibly cut total chargeback volume by 50 to 65 percent within 90 days. The 60 percent number is the midpoint and what a 100-room property at the 0.916 percent industry average should expect.

The financial math for that 100-room property: $8 million annual CNP volume, 0.916 percent chargeback rate is 73 chargebacks a year, $120 average face value is $8,760 face-value loss, $450 all-in cost per chargeback is $32,850 total annual cost. A 60 percent reduction is $19,710 in annual saving, against an investment of roughly $5,000 to $8,000 in tooling and one staff member spending two days a week on the program. The payback is under three months.

Vendor Landscape (Who Actually Does What)

The chargeback vendor market is crowded and the lines blur. For a hotel, the vendors split into three categories.

Hotel-Specific Vendors

Sertifi, Canary Technologies, and Chargeback Gurus are the three most-cited hotel-specific players. Sertifi's case study with InterContinental Buckhead Atlanta reports an 86 percent chargeback reduction following implementation, anchored in their digital authorization and signature workflow. Canary's published case studies with mid-market and select-service properties report qualitative reductions without published percentages. Chargeback Gurus operates a hospitality-focused dispute representment service with a published 80-hotel customer reporting recovered revenue at three times their prior baseline and dispute contest rate moving from 28 percent to 52 percent.

The honest framing on hotel-specific vendors: the operational tooling (digital authorization, e-signature, integrated incidents) is real value because it builds the evidence pack you would otherwise have to build by hand. The dispute representment-as-a-service is more debatable, because the marginal value over an in-house process is often the staffing cost more than the win-rate lift. Run the in-house process for sixty days first to establish your baseline, then evaluate whether the vendor lift justifies the fee.

General Chargeback Vendors

Riskified, Justt, Chargeflow, and Chargebacks911 sit at the larger payment-vendor end of the market and serve hospitality alongside other verticals. Riskified's published case study with Hotelogical reports maintained 46-plus percent dispute win rate while scaling 5x in volume with 40 percent less analyst time. These vendors integrate at the payment gateway level and bring CE 3.0 automation, deflection orchestration (RDR, CDRN, Ethoca through a single pane), and dispute response automation. Pricing typically runs as a percentage of disputes handled (10 to 20 percent of recovered revenue) plus a platform fee, which can scale into the four-figures-per-month range for a meaningful hotel.

Payment Processor Add-Ons

Stripe Radar, Adyen RevenueProtect, and the equivalent fraud-tooling at the major payment gateways are the cheapest defense against pre-transaction fraud (the criminal-fraud category rather than the friendly-fraud category). They block the obvious bad actors at the authorization step. They do not materially help with post-stay friendly fraud, which is the bulk of hotel chargeback volume in 2026. The combination of payment-processor fraud screening plus a dedicated chargeback workflow is the right stack for most independent hotels; relying only on the processor's built-in tooling leaves a meaningful gap.

The "AI Chargeback Prevention" Claim

Almost every vendor in the category now markets "AI-powered chargeback prevention". The underlying engine is almost always a combination of (a) a gradient boosting fraud-risk model at authorization, (b) rule-based deflection routing through RDR, and (c) a templated CE 3.0 representment generator. The "AI" branding is largely accurate as a label for the model component and largely inflated as a differentiator, because every serious vendor in this market is doing the same thing under the hood. If a vendor pitch leads with "proprietary AI" but cannot explain the model family, the rule structure, or the published win-rate methodology, you are buying marketing rather than substance.

A 90-Day Plan to Cut Chargebacks by 60 Percent

The plan below assumes one back-office staff member with access to the PMS, the payment gateway, and the acquirer relationship, working roughly an hour a day on the program. Cash cost: $5,000 to $8,000 over the 90 days for tooling, against a documented annual saving in the $15,000 to $25,000 range for a typical 100-room property.

Days 1 to 14. Audit the operational foundation. Pull twelve months of chargeback history from your acquirer and segment by reason code. Identify the top three codes by volume and the top three by face value (often different lists). Audit the PMS configuration for cancellation reason fields, incremental authorization trigger thresholds, and refund-to-original-card defaults. Audit the booking engine for inline policy display and explicit acknowledgment checkbox. Audit the payment gateway descriptor configuration. Document each gap. The deliverable is one written audit report that the GM and the controller both read.

Days 15 to 30. Fix the four habits. Configure the PMS to send incremental authorizations on a 50-euro or 10-percent threshold. Update the booking engine to display cancellation policy inline with rate and require explicit acknowledgment. Update confirmation email template to put policy in the first 200 characters of the body. Update payment gateway descriptor to include brand name and city in the first 16 characters plus a reachable phone number. Lock in the policy that all refunds go back to the original card of charge. Train front desk and night audit on the new workflows. Document the changes with the date of effect. This is the lowest-cost, highest-impact week of the entire program.

Days 31 to 45. Stand up the deflection stack. Subscribe to Visa RDR through your acquirer with rules for auto-refund on disputes below $50 and on reason code 13.6. Subscribe to Ethoca Alerts for Mastercard coverage. Configure the alert routing to a single back-office inbox monitored daily. Define the resolution playbook (refund inside the window for low-confidence disputes, dispute outside the window with the appropriate template). Start logging every alert outcome in a simple spreadsheet.

Days 46 to 60. Build the dispute templates. Adopt the five templates above with named documents to attach. Build a folder structure in your PMS or document store that organizes evidence by booking ID. Train one back-office person on the template-and-evidence workflow. Process every incoming chargeback against the appropriate template for the next 30 days. Log win rates per template in a simple spreadsheet.

Days 61 to 75. Stand up CE 3.0 representment. If your booking engine or PMS tracks customer login, device ID, IP at booking, and delivery address (it should), build a query that identifies, for any given dispute, the two prior undisputed transactions from the same cardholder that meet the CE 3.0 evidence requirements. If your tooling does not track these fields, configure it to start doing so immediately; the 120-day historical window means you will not benefit from this for four months but you will benefit forever after. For 10.4 disputes from repeat guests, the CE 3.0 representment is now the default response.

Days 76 to 90. Measure and tune. Pull the chargeback report for days 1 to 75 and compare to the same period a year earlier. Decompose the change by reason code. Compute total chargeback volume, total face value, total all-in cost, and the win-rate-on-disputed percentage. The 60 percent reduction will not appear in 90 days because the chargeback timeline lags the booking by 30 to 90 days, but the leading indicators (booking-engine acknowledgment rate, incremental authorization adoption, deflection alert volume, dispute win rate) should all show measurable movement. Set the cadence for what becomes the ongoing operating rhythm.

How Prostay Handles Chargebacks

Prostay Pay ships the chargeback infrastructure as a default, on the basis that an independent hotel should not have to assemble the four habits, the deflection stack, the dispute templates, and the CE 3.0 representment workflow manually.

The PMS-level incremental authorization is enabled by default with a configurable threshold (50 euros or 10 percent of estimated stay, per the lodging best practice above). The booking engine ships with inline cancellation policy display and explicit acknowledgment checkbox baked into the rate selection step. The confirmation email template places the policy in the first 200 characters of the body with the property phone number reachable.

The payment gateway descriptor is configured automatically to include the property's recognizable brand name and city in the first 16 characters, plus the front-desk phone number. Refunds are processed back to the original card by default, with cash and future-stay credit available as explicit alternative paths that warn the operator they do not protect against 13.6 disputes.

The deflection stack (Visa RDR plus Ethoca Alerts) integrates natively through the acquirer relationship and routes alerts into the Prostay back-office inbox. Resolution rules are configurable per-property with sensible defaults (auto-refund below $50, auto-refund on 13.6, manual review above $200, etc.).

The dispute representment workflow ships with the five templates above as default evidence packs. For each incoming chargeback, the system identifies the reason code, pulls the named documents from the booking record, and presents the evidence pack for human review before submission to the acquirer. CE 3.0 representment is automatic for repeat-guest cases where the two prior undisputed transactions with matching elements exist in the dataset.

The 7/14/30/60/90 day MAPE-equivalent metric for chargebacks is the rolling 90-day chargeback rate against the rolling 90-day CNP volume, surfaced in the revenue dashboard alongside the VAMP ratio with a configurable alert threshold.

None of which is to say Prostay is the only way to do this. A hotel running any modern PMS, any payment gateway, and any acquirer relationship can execute the 90-day plan above manually with effort. The practical observation is that the operational tax of building it manually adds up to four to six weeks of focused work per property per year, plus the ongoing maintenance of a system most independent hotels do not have the staffing to maintain reliably. A platform that ships the foundation by default removes the operating tax, so the back-office team can spend the time on the cases that actually need human judgment rather than producing the evidence packs from scratch each time.

Key Takeaways

Hotel chargebacks went from a rounding error to the most-watched category in payments between 2023 and 2024, with the rate jumping 816 percent to 0.916 percent and the average face value at $120 (the highest of any industry). The all-in cost per chargeback for travel and hospitality is approximately $450, or 3.75 times face value. Friendly fraud accounts for 75 to 79 percent of the volume. The VAMP rule changes that took effect in 2025 with stricter thresholds in January 2026 add a $10 per-transaction penalty and a 0.9 percent excessive merchant threshold that the typical hotel is now within touching distance of.

Nine reason codes cover ninety-five percent of independent hotel chargebacks: Visa 10.4 (Other Fraud Card-Absent), 13.1 (Not Received), 13.3 (Not as Described), 13.5 (Misrepresentation), 13.6 (Credit Not Processed), 13.7 (Cancelled Services), and Mastercard 4853 (catch-all with subcase No-Show Hotel Charge), 4855 (Not Provided), 4837 (No Authorization). Each requires different evidence. Sending the wrong evidence is the most common reason hotels lose disputes they would otherwise win.

The four chargeback-generating habits in your hotel right now are: policy not signed or surfaced, pre-authorization mishandling (no incremental authorizations, settlement above the 15 percent rule), refund processed off-card or not promptly, and vague descriptor on the cardholder statement. All four are fixable with configuration changes, not engineering projects. All four are documented in vendor case studies as the largest single levers.

The five dispute templates that win are: No-Show Charge, Stay Occurred but Disputed, Damage or Incidental, Cancellation Policy, and Resort Fees or Add-On. Each is named for its target reason code and lists the documents to attach. The single most important shift in 2026 is Visa CE 3.0 representment on 10.4 disputes for repeat-guest hotels, which wins at above 80 percent when the two prior undisputed transactions and matching data elements are available.

The pre-chargeback deflection stack (Visa RDR plus Ethoca Alerts, optionally with Verifi CDRN) pays back at seven to ten avoided chargebacks per month for a typical independent hotel, with the math getting stronger as VAMP enforcement tightens. Vendor "AI chargeback prevention" claims are largely gradient boosting at the authorization step plus rule-based deflection routing plus templated CE 3.0 representment; the engineering is fine, the differentiation is mostly marketing.

The 60 percent reduction in the title decomposes into authorization hygiene (15 to 20 percent), policy disclosure (10 to 15 percent), pre-chargeback deflection (15 to 20 percent), and CE 3.0 representment (10 to 15 percent). For a 100-room property at the industry average rate, this translates to roughly $19,710 in annual saving against $5,000 to $8,000 in tooling investment, payback under three months.

The 90-day plan in this article is the recommended starting point. Prostay ships the four habits, the deflection stack, the dispute templates, and the CE 3.0 representment workflow as defaults, which removes the operating tax of building the system manually. A live demo is the fastest way to see whether that baseline matches how you actually want to operate.